hapabapa

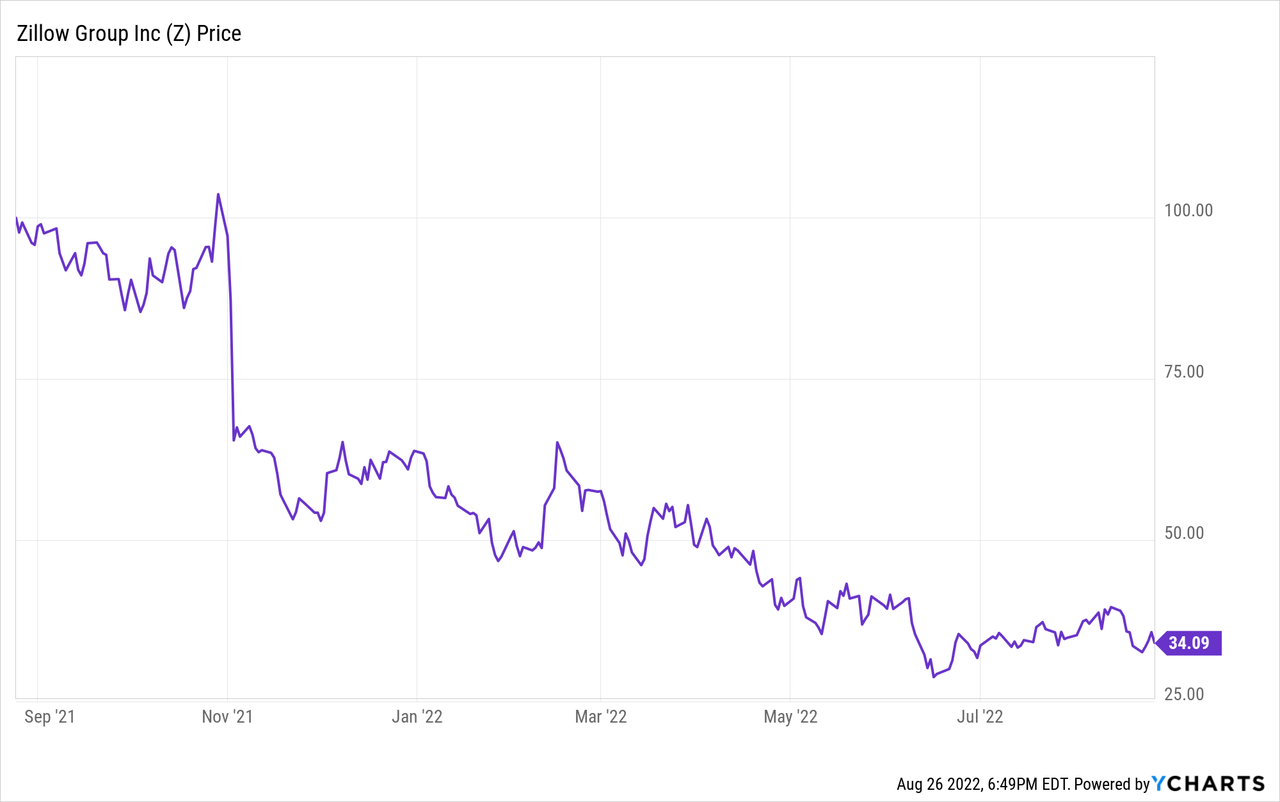

Zillow’s (NASDAQ:Z) (NASDAQ:ZG) inventory value chart over the previous 12 months has been practically a vertical line down. Provided that, it has admittedly been exhausting to belief that this actual property web titan has a path ahead, however I proceed to be an unabashed believer on this title. The market has been in an excessive amount of of a knee-jerk state over the previous 12 months, and any whiff of unhealthy information sends shares spiraling down far additional than fundamentals ought to allow.

Yr to this point, shares of Zillow have misplaced practically 50% of their worth. Losses prolonged after the corporate not too long ago launched Q2 outcomes, which, admittedly, carried solely unhealthy information (although nothing too surprising, given present macro circumstances). Whereas there may be short-term ache right here, I proceed to imagine in Zillow’s long-term prospects and stay bullish on the title.

Zillow, after all, just isn’t resistant to the gyrations of the actual property trade – which is and all the time has been massively cyclical. The corporate’s fundamental income stream, Premier Agent, depends straight on actual property brokers efficiently closing actual property transactions. All of the playing cards within the deck are stacked towards actual property proper now: charges are rising, the Fed is turning into extra hawkish, stock stays tight, and housing affordability stays a nationwide problem. On high of this, the looming danger of a recession, in addition to widespread layoffs and hiring freezes, are inflicting many would-be homebuyers to step to the sidelines.

One further non-macro draw back that traders could also be digesting is that Zillow determined to basically top-up stock-based comp for its workers. Because of Zillow’s falling share value, the corporate famous that for a lot of workers compensation is not assembly expectations or falls beneath market requirements. The one-time reset is predicted to trigger 2% dilution to the corporate’s total market cap, which it intends to appropriate over time through share repurchases.

However amid all this noise, we nonetheless must acknowledge what Zillow is: the premier website for actual property information and analysis. To place the working example right here, regardless that Zillow’s income began declining in Q2 pushed by decrease transactional exercise, common month-to-month guests in addition to complete website visits nonetheless grew by 2% y/y and 5% y/y , respectively. The truth that practically 3 billion folks go to Zillow.com or considered one of its subsidiary websites per quarter is a staggering datapoint reflecting the corporate’s near-monopoly over on-line actual property information.

Zillow visits information (Zillow Q2 shareholder letter)

Right here is my full long-term bull case for Zillow:

- Exit from iBuying shines the highlight on margin-rich IMT phase. In 2021, Zillow’s core IMT phase (which generates charges from actual property brokers discovering shoppers on the Zillow website) noticed its adjusted EBITDA margins develop to 45%, up from 38% in 2020. That signifies a income stream that’s practically pure revenue and really minimal overhead, and straight correlated with the uptick in actual property exercise. To me, eradicating the distraction from iBuying and its horrendous quarterly losses can have the impact of increasing valuation multiples for Zillow’s worthwhile core enterprise.

- Throughout Zillow, Trulia, StreetEasy, and Hotpads, just about each American shopper fascinated with shopping for or renting a house will come throughout one of many Zillow Group’s web sites. Zillow has constructed an ecosystem wealthy with actual property information that has grow to be the forefront of on-line actual property for customers. Zillow site visitors reached a document excessive of 10.2 billion visits (+6% y/y) in 2021. In 2022, website visits are nonetheless rising at a mid-single digit web page

- Zillow is a platform that may add a complete suite of further monetizable providers. With all this site visitors, Zillow’s potential to generate tertiary income is broad. At the moment, the vast majority of Zillow’s enterprise comes from promoting charges paid by actual property brokers, however the firm can also be increasing into distributing mortgage merchandise as properly. Sooner or later, Zillow may supply a full suite of “after-market” residence add-ons, together with home insurance coverage, shifting providers, furnishing/inside ornament providers, and others.

- Money wealthy. In contrast to different struggling tech firms dealing with the mouth of a possible recession, Zillow’s years of profitability have left the corporate in a robust place. Zillow at the moment has ~$3.5 billion of money (and ~$1.8 billion in web money, after contemplating debt) on its books.

Long term, Zillow is not going anyplace. Keep lengthy right here and use the dip as a shopping for alternative.

Q2 obtain

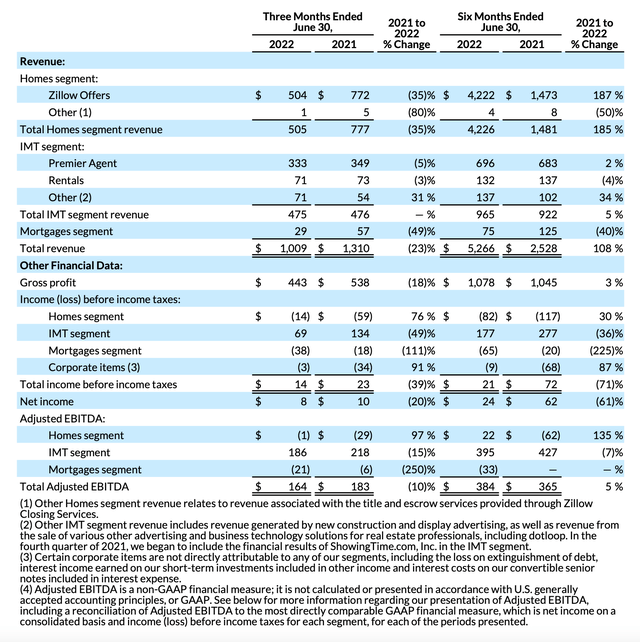

Let’s now undergo Zillow’s newest Q2 ends in higher element. The Q2 earnings abstract is proven beneath:

Zillow Q2 outcomes (Zillow Q2 shareholder letter)

Zillow’s complete income fell -23% y/y to $1.01 billion within the quarter, largely pushed by the corporate’s continued unwinding of the Zillow Affords/”Houses Section” enterprise, which noticed income decline -35% y/y to $505 million.

Apparently, the corporate signed a brand new multi-year partnership with Opendoor to supply immediate money residence presents to Zillow’s website guests. This characteristic basically replaces Zillow Affords’ earlier performance whereas placing all of the steadiness sheet danger outdoors of the corporate. The partnership stipulates that Zillow will get a reduce of any leads it sends to Opendoor, basically giving the corporate a model new “free” income stream that’s extremely synergistic with its current internet site visitors.

The large disappointment within the quarter, nevertheless, was within the IMT (web, media and know-how) phase which can grow to be Zillow’s mainline income stream after the Houses exit. Premier Agent, Zillow’s core income generator, noticed a -5% y/y income decline – which is on the low finish of the corporate’s expectations. This was pushed, after all, by the weakening housing market.

This is some useful commentary from Zillow’s CEO Wealthy Barton on what the corporate is seeing out there (key factors highlighted), taken from his ready remarks on the Q2 earnings name:

As we previewed final quarter, the housing market is rebalancing after a pandemic-fueled couple of years that had been characterised by low rates of interest, robust buyer demand and traditionally low stock ranges. We’re in a really totally different market in the present day. Affordability has grow to be very difficult for patrons. The compounding of unprecedented residence value appreciation over the previous few years and a speedy enhance in mortgage charges has resulted in new mortgage funds relative to revenue spiking again to close 2006 peak ranges. This quickly altering affordability image has impacted residence customers’ potential to search out an reasonably priced and a suitable choice, driving purchaser sentiment to a 20-year low. Decreased purchaser demand has cooled the beforehand crimson scorching sellers’ market.

Throughout the trade, we’re seeing value development meaningfully soften on pending gross sales and new mortgage purposes with for-sale stock ranges rising as houses spend extra time in the marketplace. In the end, when combining all of those elements, the housing trade complete transaction greenback quantity was flat year-over-year in Q2, whereas numerous main indicators deteriorated. Regardless of demand indicators stabilizing in July in comparison with June, we count on second half 2022 complete trade transaction quantity to meaningfully contract year-over-year.

Regardless of a difficult housing setting that we can not management, we’re as assured as ever in what we are able to management, executing on a method and a product street map that we imagine will drive outsized transaction share positive factors, outsized income per transaction and worthwhile development over time. Earlier this 12 months, we launched a product street map in a set of 2025 monetary targets which are oriented round growing engagement, growing transactions and growing income per transaction. The trail to attaining these targets and starting to construct out our imaginative and prescient includes product initiatives inside 5 development pillars: financing, touring, vendor options, integrating our providers and enhancing our companion community.”

Barton moreover famous that with macro headwinds bearing down on the corporate, the corporate is relieved that it made the choice to exit the Zillow Affords enterprise, noting that with out the steadiness sheet danger, Zillow is well-capitalized to climate a downturn.

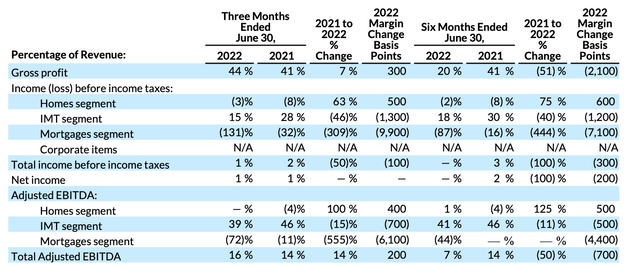

Moreover, we be aware that by shrinking losses within the Houses phase, Zillow’s total EBITDA margins are up. Whole adjusted EBITDA hit a 16% margin this quarter, up two factors from 14% within the year-ago Q2; although the Premier Agent weak spot did shrink IMT phase adjusted EBITDA by seven factors.

Zillow adjusted EBITDA (Zillow Q2 shareholder letter)

Key takeaways

Investing in Zillow would require each a robust abdomen for near-term volatility in addition to a capability to “zoom out” and have a look at the unbelievable know-how and information belongings that it has constructed up and has the flexibility to monetize. Actual property will not be in a downturn eternally, and so long as Zillow stays the dominant website for actual property internet site visitors, actual property brokers will proceed to anchor on Zillow as their major lead-gen platform. Proceed scooping up this inventory because it falls.