- Mortgage funds are increased than hire in 45 of the 50 largest U.S. metros, up from 22 in 2019.

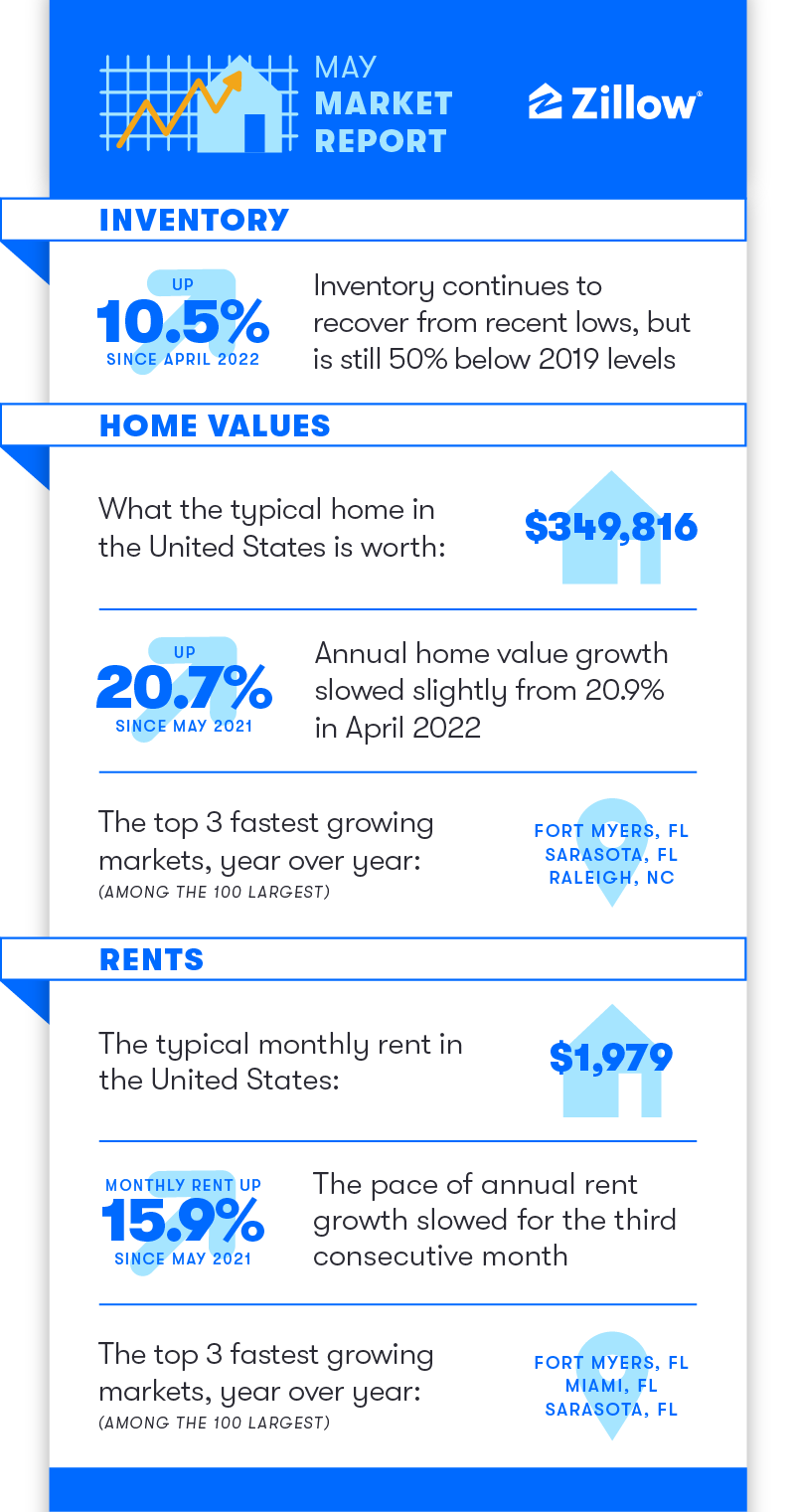

- Value appreciation is lastly beginning to sluggish, easing barely from 20.9% annual development in April to twenty.7% in Might.

- Stock continues to get well from February lows, however continues to be 50% beneath 2019 ranges.

Ballooning mortgage prices, pushed by skyrocketing costs and rates of interest, have made mortgages much less reasonably priced than at any time since a minimum of 2007. Demand for properties has pulled again in response, easing value development, slowing gross sales and boosting stock.

Mortgage charges shot up in early June, averaging 5.78% as of Thursday. The acquisition of a typical U.S. residence [1] at that fee would imply month-to-month mortgage funds of $2,127 – that’s 51% increased than a 12 months in the past and up 36% 12 months thus far.

Incomes are lagging additional behind fast-rising mortgage prices, resulting in essentially the most vital affordability challenges prior to now 15 years. The most recent affordability information accessible from April exhibits month-to-month funds [2] taking about 28% of house owners’ month-to-month revenue — dangerously near the 30% threshold, past which is taken into account a price burden. Zillow information for this metric is on the market by way of 2007; the Atlanta Federal Reserve’s Residence Possession Affordability Monitor exhibits affordability bottoming out in July 2006.

Though rents have soared because the begin of 2021, the quickly rising price of a mortgage nonetheless makes hire the cheaper possibility almost in all places. A typical hire cost in Might is costlier than a mortgage cost (with a 20% down cost), together with taxes and insurance coverage, in simply 5 of the 50 largest U.S. metros. In Might 2019, hire was costlier in 28 of these metros.

Consumers lastly balk

Value appreciation, based on the Zillow Residence Worth Index (ZHVI), lastly turned the nook after setting new file highs for 13 straight months, as its annual development fee dipped from 20.9% in April to twenty.7% in Might. The standard U.S. house is now price $349,816 — almost $60,000 greater than final 12 months and nearly $95,000 increased than in Might 2020.

The most popular annual appreciation among the many 50 largest U.S. metros may be seen in Raleigh (37.3%), Tampa (36.5%), and Orlando (33,4%). The slowest annual residence worth development is in Washington D.C. (10.2%), Baltimore (11.1%) and Pittsburgh (11.8%).

It’ll take time to substantiate, however for now the pattern seems to indicate that the market handed an inflection level for residence values between April and Might, transitioning from ever-hotter to somewhat-cooler value development. This deceleration is a transparent sign that patrons are dialing again their demand for properties within the face of daunting affordability challenges.

The variety of for-sale listings that went below contract in Might is down almost 20% from 2021, when that exercise was close to a four-year peak, and is 2% beneath that of Might 2019. The median time on marketplace for new listings is simply seven days — holding regular from April and even with final Might.

Stock continues to get well

Whole stock of for-sale listings continued its regular spring climb, marking 10.5% development over April, and now sits simply 14.2% beneath its year-ago stage. Nonetheless, new listings are rising at a slower tempo: 5.6% month-over-month development. This probably means listings are starting to hold across the market longer and this slowdown is contributing to the restoration of stock.

And whereas extra complete stock is encouraging for patrons confronted with stiff competitors and bidding wars in months prior, there are nonetheless 50% fewer listings to select from than in Might 2019, earlier than the pandemic.

Rents rising quick

Typical rents are as much as $1,979 within the U.S. and nonetheless rising quick, with 1.2% month-to-month development that barely edged April’s 1.1% month-over month rise. To place this into context, the typical month-to-month Might hire development from 2014 to 2019 was 0.7%. Annual hire appreciation for Might is 15.9%, easing off a peak of 17.2% in February.

Florida nonetheless tops the hire development leaderboard, with rents rising the quickest yearly in Miami (31%), Tampa (25.2%), and Orlando (23.7%) of all main metros. The slowest 12 months over 12 months development is discovered within the Midwest and Rust Belt: Minneapolis (6.5%), Milwaukee (7.5%), and Pittsburgh (8.4%).

Trying ahead

The market deceleration has led to a downward adjustment for Zillow’s forecast for one-year residence value appreciation since April. The Zillow Residence Worth Index (ZHVI) is predicted to extend 9.7% within the twelve months ending in Might 2023, in comparison with final month’s forecast of 11.6% within the twelve months ending April 2023.

[1] Assuming a brand new mortgage on a home priced at Zillow’s Residence Worth Index in Might of $349,816, utilizing a 20% down cost and a 30-year fixed-rate mortgage at 5.78%, contains taxes and insurance coverage

[2] Assuming a brand new mortgage on a home priced at Zillow’s Residence Worth Index in April of $344,773, utilizing a 20% down cost and a 30-year fixed-rate mortgage at 4.98%, contains taxes and insurance coverage