MoMo Productions/DigitalVision by way of Getty Pictures

Our intention for this paper is to evaluate the attractiveness of Zillow at this time, with an emphasis on assessing the well being of the housing market. Though Zillow has a aggressive benefit relative to its opponents, its fortunes are closely correlated with the well being of the housing market and, in extension, the financial system. We’re seeing proof suggesting that the market is slowing, which is able to probably weaken returns within the close to time period.

Firm Description:

Zillow (NASDAQ:Z) is a new-age property agent, offering a platform for properties to be bought, offered and rented. Traditionally, patrons wanted to talk to varied brokers in a location to determine what properties have been out there, it was a sluggish and time-consuming course of. Then some companies determined to innovate by itemizing properties on-line. With Zillow, individuals can browse properties from the consolation of a cell app, which importantly permits for comparability of all properties listed in an space.

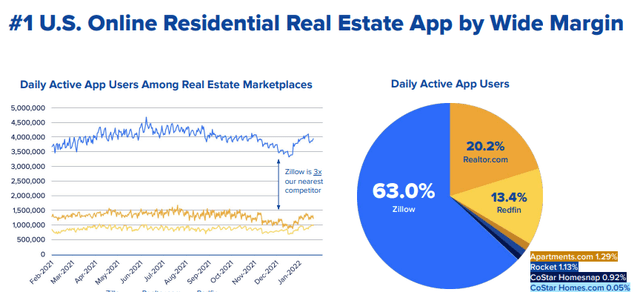

As of at this time, Zillow is by far the biggest actual property app within the US, and it’s not shut. Zillow was in a position to obtain this by offering shoppers with the functionalities they need higher than their opponents. Having a number of main apps defeats the aim and diminishes the client/vendor expertise, Zillow gained the race to construct a buyer base.

Zillow’s market dominance (Zillow)

Zillow earns nearly all of its income from the next companies:

- Residence section – This was an iBuying enterprise. This section has been shut down by Zillow, as they’ve struggled to generate an enough return. Zillow is within the strategy of liquidating the remaining properties.

- IMT section – That is the core operation of Zillow. Premier agent and leases.

- Premier brokers are SaaS instruments which permit brokers to arrange their listings and promote their companies on Zillow. Importantly, Zillow generates income from a cost-per-lead association.

- Leases are promoting companies for rental properties.

- Mortgage section – That is twofold. Firstly, Zillow is a licensed lender and so gives debtors the choice to mortgage a house they’ve discovered. Equally, Zillow permits mortgage suppliers to supply their companies, thus giving debtors a market of choices. Once more, Zillow generates income on a cost-per-lead association.

Zillow is trying to be the “Housing Tremendous App” the place all the pieces might be achieved simply in a single place, capturing income in any respect levels of the housing course of. We should say, Zillow has achieved a implausible job of maximizing the monetization of its companies. Administration clearly understands the facility Zillow has available in the market, they usually leverage that to make purchasers pay.

Present Situations:

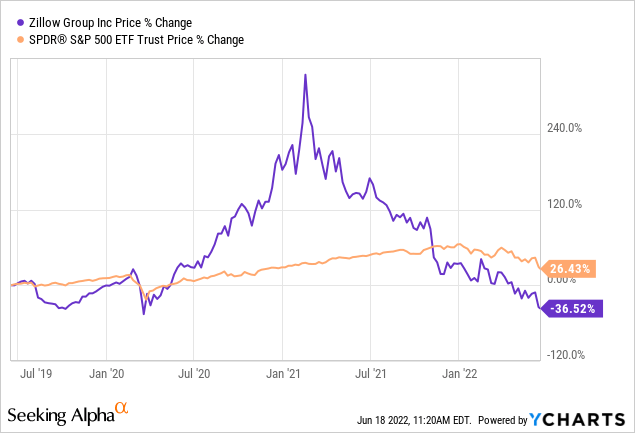

Zillow’s shares haven’t carried out so effectively in current months, falling an eye-watering 85% since Feb 2021. There are a lot of causes for this, together with the aforementioned closure of the Provides enterprise. The most important motive, nonetheless, we consider, is the financial developments within the US market.

Between Mar 2020 and Feb 2021, shares grew 666%. The rationale for this was an unsurprising growth within the housing market.

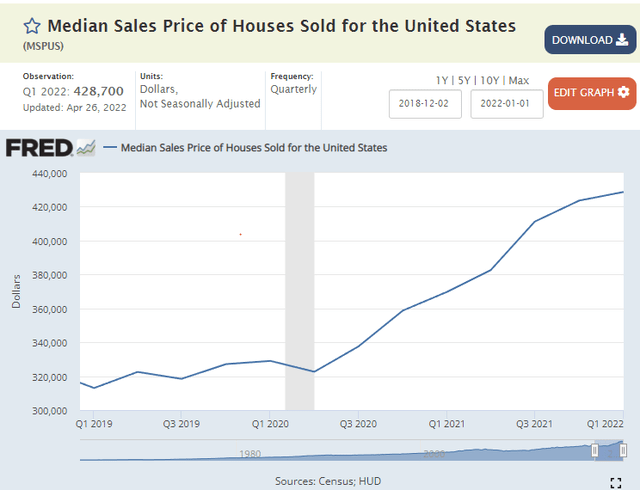

Median Gross sales Value of Homes Offered for america (FRED)

Because the above graph reveals, home costs screamed increased as provide couldn’t match demand for properties. With Zillow gaining access to varied factors of the method, revenues grew aggressively.

The problem is that the enterprise didn’t develop by 666% and so Zillow rapidly discovered itself overvalued and extremely delicate to any change in situations. As markets started cooling, Zillow started falling.

Our hesitation is that the graph above seems to be to be plateauing in Q1 2022. This implies demand is both falling or provide is catching up, provided that the US market is scuffling with a scarcity, that is probably a demand-side concern.

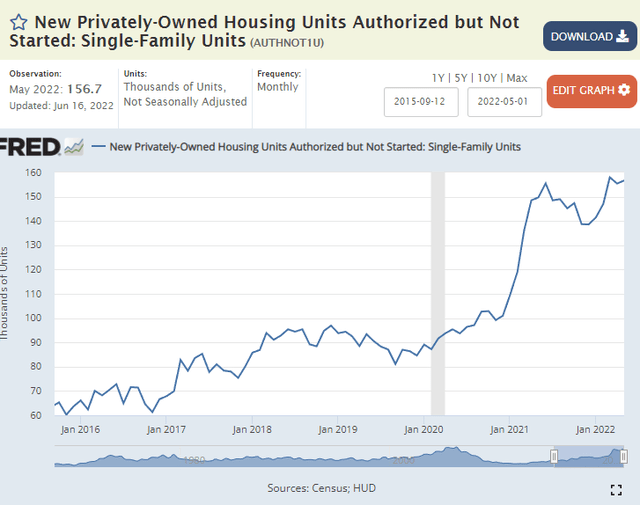

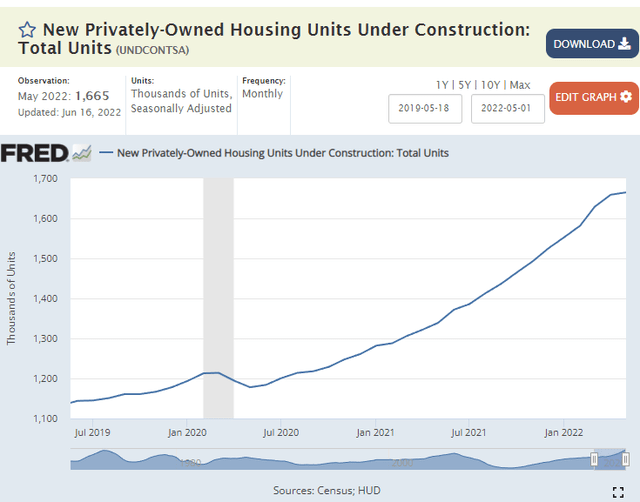

As a secondary test for the well being of the housing market, we wish to see a rising variety of approved new-build constructions and the variety of models beneath building rising. The rationale for that is that if new-builds are being approved and constructed, it is as a result of the medium-term view is that further properties will probably be required to satisfy demand on the present market worth, if not increased.

Variety of models approved (FRED) Variety of models beneath building (FRED)

What we word is that the variety of models beneath building has fallen for the primary month since COVID-19, and the variety of authorizations stabilized after the COVID-19 growth. This helps our evaluation above that the market is significantly cooling as financial situations deteriorate. That is unlikely to abruptly enhance in a single day.

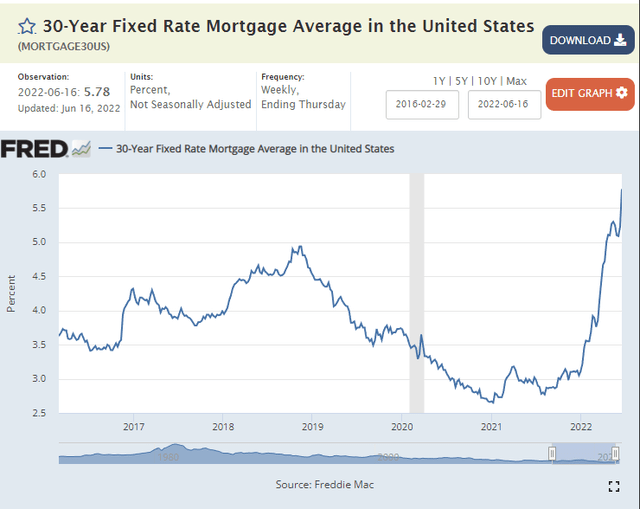

Lastly, we are able to have a look at mortgage charges. Naturally, the decrease they’re, the extra probably individuals are to maneuver.

US 30Y Mounted price (FRED)

Because the above reveals, successive rate of interest hikes have left mortgage charges hovering. On account of this, individuals’s affordability falls, except they’ll enhance their earnings by the identical quantity.

With inflation as excessive as it’s, individuals are scuffling with a cost-of-living disaster quite than having the monetary capability to maneuver residence. This has already impacted demand, with the US financial system shrinking. Analysis has proven that weakening market situations imply falling home costs as much less discretionary earnings is on the market. That is our perception of what’s more likely to come within the subsequent 12 months. This may straight influence all of Zillow’s income streams. Not less than they exited Zillow gives.

Financials:

Sadly, Zillow has been loss-making for almost all of its existence. The rationale for that is an aggressive advertising push. SG&A represents 19% of income, with GPM being 21.6% in FY21. LTM efficiency is worse, probably on the again of harder buying and selling situations (Supply: TIKR Terminal). Due to this, we’re fairly involved concerning the medium-term efficiency of the enterprise if financial situations do worsen. It’s not out of the query that losses attain $500M once more. In 2021, EBITDA was $195M with an curiosity expense of $191M. This offers Zillow an curiosity protection of 1.01, which is much from comfy. Fortunately, they sit on a money stability of $3.6BN.

Additional, Zillow introduced a share buyback program of $750M in December 2021, with an extra $1BN approved in the newest quarter. We don’t actually perceive this choice. The enterprise is asset-light and never cash-intensive, however the enterprise is loss-making. Traders could marvel why Zillow shouldn’t be targeted on fixing this as an alternative of shopping for again shares.

Trying ahead, Zillow is focusing on $5BN in income by 2025, with an EBITDA margin of 45%. That will characterize 23% progress from right here and a 6% enchancment of their EBITDA margin. We wrestle to see this taking part in out. In our evaluation of the enterprise, we anticipate to see $1.8-2BN in 2022, which is flat. That is based mostly on a discount in property gross sales however an enchancment in transactions by means of Zillow. Relating to margin enlargement, that is definitely extra potential than the income progress. Analysts are predicting income of $3.1BN in 2025 and an EBITDA margin of 39% (Supply: TIKR Terminal).

You will need to perceive that the numbers within the above paragraph are based mostly on administration’s carve-out of the separate enterprise models, because it excludes the home-buying enterprise. One further level to issue thus is the overheads of the home-buying enterprise. Now that this enterprise is gone, its prices will have to be allotted to the IMT and mortgage enterprise, which is able to considerably depress their margins. Provided that the enterprise is loss-making as a complete, there’s a likelihood that it’s going to make their core enterprise (IMT) loss-making, which is able to inevitably kill what little optimistic market sentiment stays.

Vivid Aspect:

We’ve been fairly harsh on Zillow and so want to determine three key areas of upside.

Firstly, Zillow has single-digit market share in the true property market, but dominates the net app market. This implies the digitization of the market remains to be in its early part. On account of this, they need to have the ability to maintain progress as extra enterprise is taken to on-line platforms.

Secondly, their app is genuinely excellent and standard amongst extra than simply these seeking to purchase/promote/lease. Many get pleasure from simply shopping properties, analysis into this has discovered the quantity to be at 35%. This offers Zillow beneficial information which it will probably monetize. The simple manner, after all, is promoting however they definitely have choices.

Lastly, if Zillow can work out a worthwhile mannequin, enlargement abroad is a viable choice. Though markets differ barely in the best way they do enterprise, the idea is pretty repeatable. This may enable Zillow to diversify its income away from the US housing market.

Closing Ideas:

Zillow is a real innovator who has actually shaken up an archaic trade. The enterprise has made just a few errors however that may often occur when you’re rising on the price they’re, criticism of administration over the house shopping for debacle is exaggerated. That being stated, they’re now a sufferer of their very own success. The enterprise is inherently cyclical being correlated to the housing market and, in our view, is heading in direction of a downtrend. Our perception is that the share worth correction over the past 12 months is a mirrored image of the market realizing that this isn’t one other tech enterprise which is able to develop at double digits ceaselessly.

Zillow didn’t obtain profitability throughout an enormous housing bull market and will now endure from larger losses ought to a downturn happen. Traders who see this as a diamond within the tough ought to contemplate if optimistic worth motion will happen within the coming 12 months. We can not see something, and so it’s value ready for now.

We thus price this inventory a promote.