- Stock rose considerably in March, a welcome return to seasonal norms for the housing market.

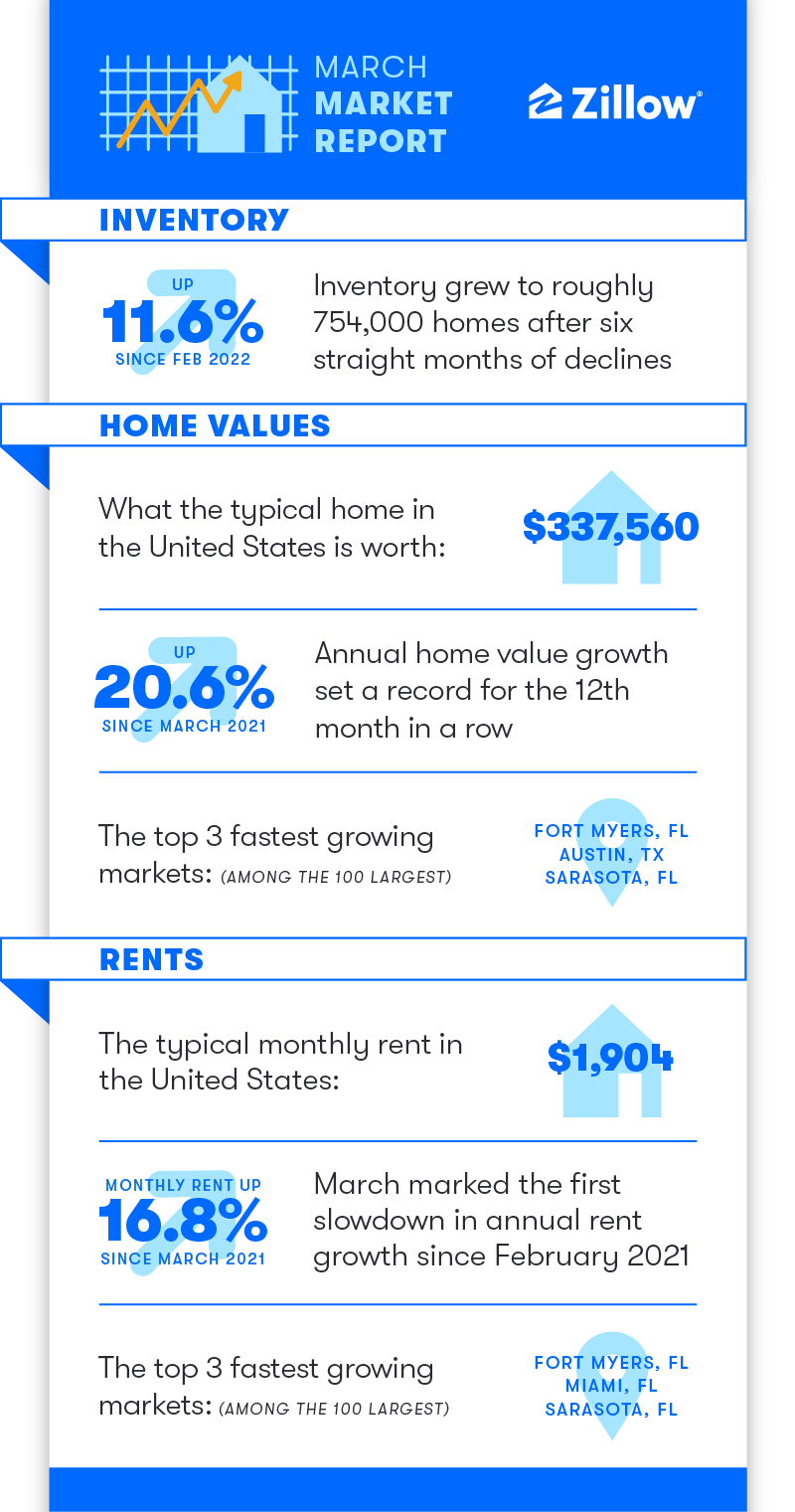

- Residence values are nonetheless rising shortly, however not accelerating on a month-to-month foundation. The standard U.S. house is price 20.6% greater than it was one 12 months in the past.

- Annual lease development slowed for the primary time in additional than a 12 months, and rents grew lower than 1% from February, suggesting slower development within the 12 months forward.

Residence customers are going through a one-two affordability punch this spring: Shortly rising mortgage charges are compounding affordability challenges which were introduced on by report residence worth development. But to date, regardless of rising prices, patrons stay able to pounce on any stock that hits the market. When the anticipated spring stock increase lastly arrived in March, the tempo and quantity of gross sales picked up in response.

Stock — the rely of energetic for-sale residence listings available on the market — lastly started to carry off in March after falling persistently since August 2021. Complete listings jumped 11.6% from February, the most important month-to-month achieve in knowledge by way of 2018, offering sufficient of a soar past seasonal norms that the market started to make somewhat progress again up from seasonally adjusted report lows. Wanting again to the primary quarter of 2019 for a pre-COVID seasonal comparability, nationwide stock this March was 52.2% under its March 2019 stage: a modestly smaller deficit than in February, when listings have been down 53.9% from the identical time in 2019.

Of the 50 largest U.S. metros, these with the biggest stock deficits relative to March 2019 are Raleigh (-70.7%), Miami (-67.5%) and Nashville (-66%). These with the smallest decreases are San Francisco (-9.2%), San Jose (-14%) and Minneapolis (-29.7%).

Consumers not deterred (but) by larger costs

The cumulative impact of months of low stock may be seen in nonetheless sturdy value appreciation. The standard U.S. house is now price $337,560 — up 20.6% from March 2021. That is the twelfth consecutive month by which a brand new report for annual value appreciation has been set.

Coupled with this 12 months’s quickly rising mortgage charges, these costs suggest a month-to-month mortgage fee of $1,316 (principal and curiosity solely, assuming a 30-year fixed-rate mortgage with a 20% down fee), which is 38% larger than in March 2021 and virtually 20% larger than a mere three months in the past.

All 50 of the nation’s largest metro areas skilled double-digit year-over-year development in March. Annual development was quickest in Austin (42.7%), Raleigh (34.9%) and Tampa (33.1%), and slowest in Washington, D.C. (11.4%), Baltimore (11.6%) and Milwaukee (11.7%). On a month-to-month foundation, development was quickest in Tampa (3.0%), Raleigh (2.8%) and Las Vegas (2.8%), and slowest in New Orleans (0.6%), Richmond (0.7%) and Windfall (0.9%). Sixteen of the 50 largest markets noticed decelerating month-to-month development in residence values, probably the most since November.

March proved to be the most important check but of whether or not sufficient patrons can meet the brand new asking costs to maintain residence values rising at a report tempo, and the reply was a convincing “sure.” Newly pending gross sales rose 11.6% in March — the very same improve as stock. The median itemizing went pending after simply 9 days — two days quicker than in February and 24 days quicker than the final March earlier than the pandemic, in 2019.

Early indicators of a rebalancing

Whereas there’s loads of gasoline within the tank as home-shopping season kicks into gear, there can be a degree when the price of shopping for a house deters sufficient patrons to sluggish value development, and indicators are rising that we could also be nearing the height for residence worth appreciation. Month-over-month value development was 1.6% for the second month in a row in March — a tempo that, if compounded for 12 months, would yield 20.7% annual development.

Newly pending residence gross sales this March lagged behind their tempo from a 12 months in the past, with 19% fewer than in March 2021, after February notched a 15% year-over-year decline. The slowdown in gross sales quantity may very well be attributable to the one-two punch of excessive costs and rising mortgage charges denting demand this spring.

A looming swing again towards a extra balanced housing market shouldn’t be confused with a market crash, which stays most unlikely. Possibly, slowing value development won’t finish with costs truly falling, and in reality, the market ought to stay scorching by historic requirements for a lot of months to return. Provide is on the upswing, and demand will finally cool as costs rise out of attain for sufficient households, however there’s a lengthy approach to go earlier than we attain a provide glut, and there’s loads of pent-up home-buying demand to work by way of.

Rental market nonetheless scorching, however modestly cooling

The for-sale market is the obvious place to look at the consequences of restricted provide, however the rental market shouldn’t be immune, both. Residence customers, particularly ageing millennials, who strike out in in the present day’s aggressive and sparse for-sale market are more likely to keep renters longer. On the identical time, the big Era Z cohort is starting to enter the rental market. Largely due to these two elements, this excessive rental demand is maintaining rental emptiness charges close to all-time lows and pushing lease costs — after a quick, early pandemic pause — up at an virtually equally quick tempo as residence values.

Rents in March rose 0.7% from February and 16.8% from a 12 months earlier. That marks a slight deceleration in each month-to-month and annual lease development, after February’s record-high 17.2% year-over-year development. Typical lease throughout the U.S. is now $1,904 monthly, $295 larger than in March 2020. Hire development was sluggish in 2020 after the outbreak of the pandemic, however skyrocketed in 2021. Florida metro areas made a clear sweep on the rostrum for quickest annual lease development in March: Miami (32.6%), Tampa (28.1%) and Orlando (24.7%) had the fastest-growing rents of the 50 largest U.S. metros. Colder markets noticed the slowest year-over-year development in March: Minneapolis (7.0%), Milwaukee (7.6%) and Pittsburgh (8.9%) introduced up the rear.

Wanting forward

Zillow’s residence worth forecast now requires 14.9% development by way of March 2023, down from a year-ahead forecast of 16.5% development made in February. Zillow’s present residence gross sales forecast has been lowered as nicely, to six.09 million gross sales in 2022, which might mark a slight decline of 0.5% from 2021. Affordability headwinds have strengthened quicker than anticipated, largely resulting from sharp will increase in mortgage charges, resulting in the downwardly revised forecast. Nonetheless, these figures would signify a remarkably aggressive housing market within the coming 12 months. Annual residence worth development of 14.9% would have been the best ever recorded by Zillow earlier than June 2021, and 6.09 million present residence gross sales would mark the second-best calendar 12 months whole since 2006.