SolStock/E+ through Getty Photos

Clothes and different attire will be an attention-grabbing house if you could find the fitting corporations to purchase into. Typically, one of the simplest ways to do that is to concentrate on area of interest suppliers. And one nice instance of this may be seen by trying at Carter’s (NYSE:CRI), which is the biggest branded marketer in North America of attire aimed solely towards infants and younger youngsters. This business chief doesn’t, sadly, have a constantly rising working historical past. However it does have a historical past of engaging money flows and shares are buying and selling at pretty low-cost ranges presently. All issues thought of, the corporate appears to supply an honest quantity of upside potential. And as such, I’ve determined to charge it a delicate ‘purchase’ presently.

Garments for little ones

As I discussed already, Carter’s is the biggest branded marketer of attire for infants and younger youngsters on this continent. The corporate does this via quite a lot of manufacturers that it owns, together with two megabrands: Carter’s and OshKosh B’gosh. Below the Carter’s model, the corporate focuses on high-quality attire and equipment for youngsters starting from new child measurement to age 14. The OshKosh model focuses on the identical demographic, besides that its emphasis is on attire and equipment. Specifically, it additionally has a particular focus relating to play garments for toddlers and younger youngsters.

At current, the corporate additionally has a couple of different manufacturers beneath its belt. One in all these is Skip Hop, which operates as a number one child and younger little one way of life model. Below the Little one of Mine banner, the corporate sells its Carter’s merchandise solely to Walmart (WMT). Related preparations have been made with different retailers. As an illustration, the corporate does the identical factor with Goal (TGT) beneath the Simply One You banner, whereas for Amazon (AMZN) the model identify used is Easy Pleasure. One other attention-grabbing model is Little Planet, which focuses on offering sustainable clothes via the sourcing of largely natural cotton. Like lots of the firm’s different strains of merchandise, it focuses totally on child attire and equipment. It additionally has its fingers in sleepwear and reward bundles. It is also price noting then the corporate does generate a few of its income from licensing its manufacturers to its companions. In the event you ever see one among its model names on footwear, outerwear, hair equipment, jewellery, toys, paper items, dwelling decor, cribs, child furnishings, or bedding, then it’s virtually definitely a state of affairs of the corporate licensing out its merchandise to a 3rd occasion.

Creator – SEC EDGAR Information

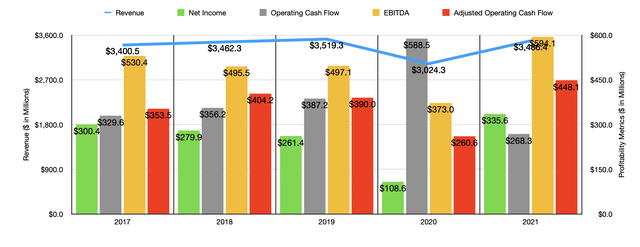

For a lot of the previous 5 years, the general trajectory for the corporate’s income has been constructive. Income rose from $3.40 billion in 2017 to $3.52 billion in 2019. The COVID-19 pandemic pushed income right down to $3.02 billion in 2020. However that decline was short-lived, with gross sales climbing to $3.49 billion final 12 months. This isn’t to say that each one is effectively with the corporate. In truth, the agency is experiencing some weak point in gross sales this 12 months. For the primary half of the 12 months, income totaled $1.48 billion. That is down from the $1.53 billion generated within the first half of the 2021 fiscal 12 months. Based on the information supplied, this 3.4% lower in income 12 months over 12 months was pushed largely by decreased web gross sales related to the corporate’s U.S. Retail section. This isn’t to say the whole lot on that entrance was dangerous. Web gross sales within the unique Carter’s manufacturers, mixed with energy all through Canada and thru the worldwide wholesale channels, finally elevated. However these enhancements simply weren’t sufficient to offset the weakening market right here at dwelling.

In the case of profitability, the image for the enterprise has been a bit extra sophisticated. Between 2017 and 2020, web revenue for the agency fell 12 months after 12 months, declining from $300.4 million to $108.6 million. However then, in 2021, profitability shot as much as $335.6 million. Different profitability metrics, in the meantime, have typically been constructive. Working money movement, as an illustration, rose between 2017 and 2020, ultimately dropping although from $588.5 million in 2020 to $268.3 million final 12 months. If we alter for modifications in working capital, nevertheless, it could have risen from $260.6 million in 2020 to $448.1 million final 12 months. Over that very same window of time, EBITDA has additionally been risky. However what’s most necessary is that the metric finally hit $594.1 million final 12 months for what was an at-least five-year excessive.

Creator – SEC EDGAR Information

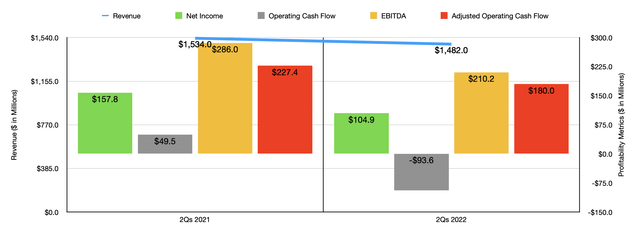

As you would possibly anticipate, profitability up to now this 12 months has taken a step again. Web revenue within the first half of the 12 months totaled $104.9 million. That is down from the $157.8 million we get utilizing 2021 outcomes. Despite the fact that income decreased for the corporate, its value of products offered managed to rise 12 months over 12 months, climbing by 1.2% in all. That, offset some by antagonistic buy commitments, assist to push the corporate’s gross revenue margin down from 49.6% to 46.3%. On the material buy dedication aspect, administration stated that they booked a cost on account of lowered ahead stock commitments aimed toward higher aligning with decrease demand forecasts. It additionally concerned elevated stock provisions and different associated modifications. As well as, the corporate additionally skilled a rise in transportation prices, largely related to its U.S. Wholesale section. This may very well be an indication of additional ache to come back. You see, 12 months over 12 months, the corporate elevated its stock reserves by 14.8%, with complete inventories rising by 38.5%. This follows an identical pattern seen with some main retailers lately, indicating that extra inventories would possibly finally weigh on profitability for the close to time period. Naturally, because the chart above illustrates, these points have additionally negatively impacted the corporate’s different profitability metrics like working money movement, adjusted working money movement, and EBITDA.

Creator – SEC EDGAR Information

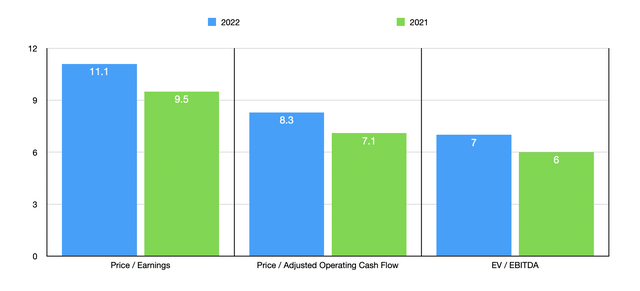

In the case of the 2022 fiscal 12 months as an entire, administration does assume that income will are available at between $3.25 billion and $3.30 billion. This does suggest continued weak point for the remainder of the 12 months. As a part of this, earnings per share ought to are available between $7.10 and $7.60. On the midpoint, that will suggest web revenue of $286.6 million. That is fairly a decline from the $335.6 million reported final 12 months. If we annualize outcomes achieved up to now this 12 months for the opposite profitability metrics, we must always anticipate adjusted working money movement of $382.7 million and EBITDA of roughly $507.4 million. Even with these declines, shares of the enterprise are attractively priced. The ahead worth to earnings a number of of the corporate must be 11.1. That compares to the 9.5 studying we get utilizing 2021 outcomes. The worth to adjusted working money movement a number of ought to rise from 7.1 to eight.3, whereas the EV to EBITDA a number of ought to enhance from 6 to 7. To place this all in perspective, I in contrast the corporate to 5 related companies. On a ahead price-to-earnings foundation, these corporations ranged from a low of 9.5 to a excessive of 34.8. Two of the 5 corporations have been cheaper than our prospect. Utilizing the worth to working money movement strategy, the vary was from 8 to 13.8, with solely one of many corporations cheaper than Carter’s. And in relation to the EV to EBITDA strategy, the vary was from 8 to 10, with our prospect being the most cost effective of the group.

| Firm | Worth / Earnings | Worth / Working Money Circulation | EV / EBITDA |

| Carter’s | 11.1 | 8.3 | 7.0 |

| Hanesbrands (HBI) | 9.5 | 8.0 | 10.0 |

| Ermenegildo Zegna N.V. (ZGN) | 34.8 | 12.3 | 9.9 |

| Below Armour (UAA) | 16.5 | 13.8 | 9.6 |

| Kontoor Manufacturers (KTB) | 10.0 | 9.0 | 8.0 |

| Canada Goose Holdings (GOOS) | 15.8 | 10.8 | 9.5 |

Takeaway

Operationally talking, Carter’s appears to be doing fairly effectively contemplating latest financial points. Having stated that, this 12 months can be considerably painful for the enterprise in comparison with what final 12 months was. It is also attainable, relying on how dangerous issues get, that this ache may worsen additional subsequent 12 months. However that’s extremely speculative. Assuming the image does not get a lot worse, shares of the corporate do look to be buying and selling on a budget on an absolute foundation and are even buying and selling on the decrease finish of the spectrum in comparison with related companies. I’m considerably unnerved by the historic efficiency of the agency from a profitability perspective. However all issues thought of, I do consider a delicate ‘purchase’ ranking for the corporate is acceptable presently.