")

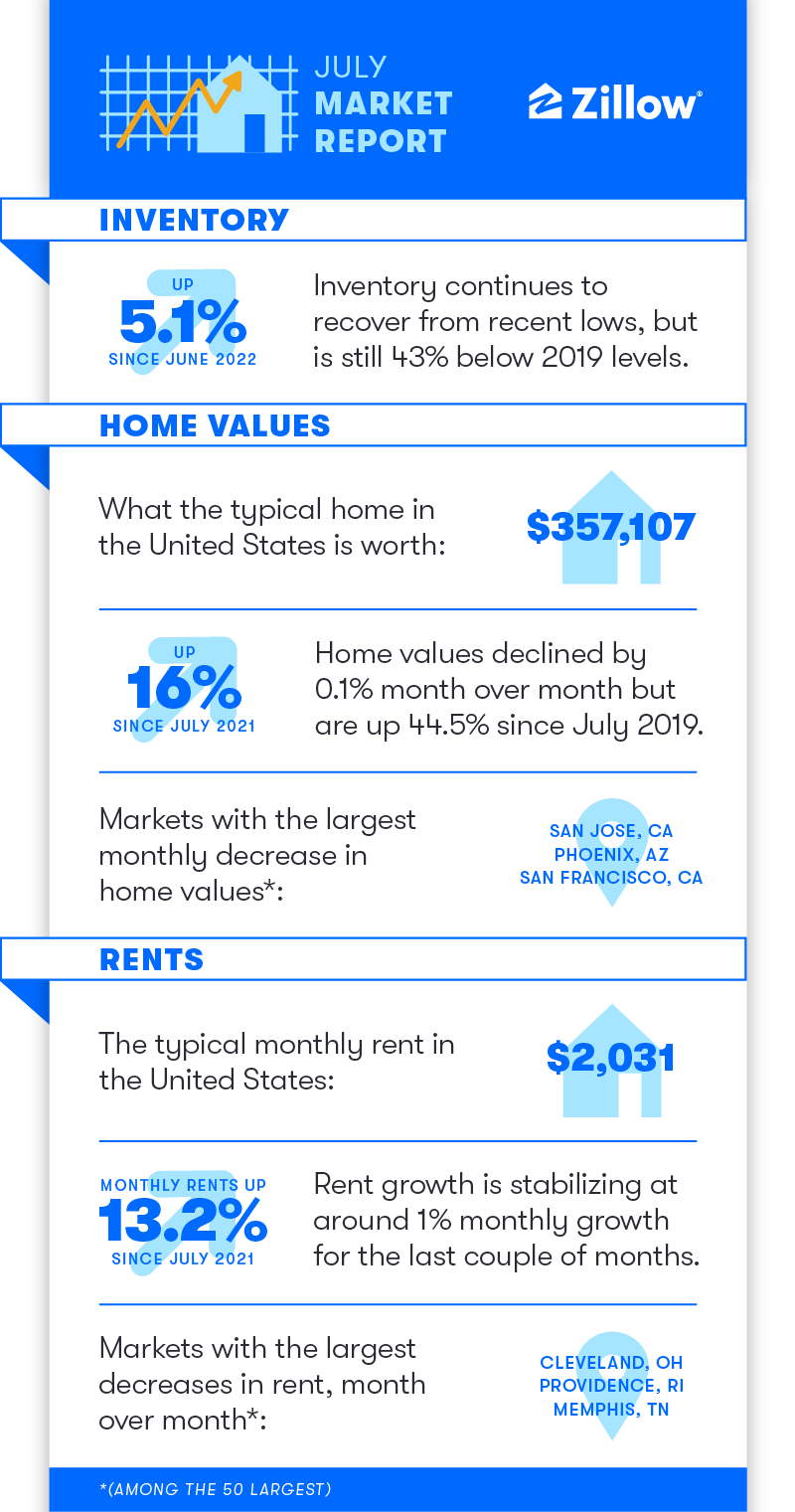

- U.S. residence values fell 0.1% from June to July, the primary decline within the uncooked Zillow House Worth Index since 2012. House values fell final month in 30 of the 50 largest metro areas, however are nonetheless up 16% from a 12 months in the past.

- Rising stock is being pushed by properties lingering available on the market and new listings trailing pre-pandemic ranges. It took 10 days for a list to go pending in July, two days longer than in June.

- Hire appreciation is slowing, however the development charge stays a lot increased than pre-pandemic ranges

After two years of unprecedented development, nationwide residence values fell barely month-over-month for the primary time since 2012, the 12 months residence values hit a trough after the housing bubble and bust of the aughts. Whereas July’s housing market information replace is huge information, and will get first-time patrons’ hopes up, the longer term is unlikely to convey significant enchancment to housing affordability.

Costs fall for the primary time in a decade

The everyday U.S. residence worth now stands at $357,107 after declining by 0.1% ($366) month over month in July, as measured by the uncooked Zillow House Worth Index (ZHVI). A extra responsive, but in addition extra unstable taste of Zillow’s headline value index – month-to-month development within the uncooked ZHVI – has relaxed since reaching a latest peak in April of 1.9% (a charge that may annualize to a whopping 25.1%), slowing to 1.2% development (15.3% anualized) in Might and 0.8% development (9.7% annualized) in June.

House values measured by uncooked ZHVI fell from June to July in 30 of the 50 largest metro areas, a rise from 13 metros the earlier month. The most important month-to-month residence worth declines had been in San Jose (-4.5%) and San Francisco (-2.8%, that’s -28.7% anualized) — the nation’s costliest main markets — adopted by Phoenix (-2.8%) and Austin (-2.7%), which noticed probably the most excessive development over the pandemic. Values elevated probably the most from June in Miami (1.5%, a nonetheless aggressive 19% annualized charge), Richmond (1%, 12.1% annualized) and Memphis (0.9%, 11.2% annualized), though month-to-month development is decelerating in these markets as properly.

Whereas the latest decline in costs is a notable growth, the housing market remains to be removed from a return to “regular” situations. The present slowdown is prompted by the collision of utmost value development through the early- and mid-pandemic with the sudden improve in mortgage charges since December – a mix that swiftly weakened would-be homebuyers’ capacity to afford or qualify to buy their subsequent home. The nation’s typical residence worth remains to be up 16% 12 months over 12 months and 44.5% since July 2019, regardless of softer pricing in more moderen months. Incorporate increased mortgage charges, and the standard mortgage cost has risen by greater than 60% in only one 12 months. Whereas excessive costs plus increased mortgage charges have pushed some patrons from the marketplace for now, these customers who’re in a position to proceed immediately face a a lot much less aggressive market, providing them extra time to conduct their search and extra choices to think about.

Stock will increase proceed as properties take longer to promote and sellers minimize costs

Cooling competitors amongst patrons has resulted in properties spending extra time available on the market earlier than promoting. Whereas the standard residence that goes below contract nonetheless does so in a traditionally quick period of time, this market velocity has slowed significantly from the fast tempo set earlier this 12 months. Properties went pending in a median of 10 days in July – two days slower than the median tempo in June. Properties lingering available on the market proceed to push for-sale stock up, whilst the speed of recent properties coming into the market slows. The variety of lively for-sale listings through the month elevated by 5.1% in July from June. The rise was the fifth consecutive month-to-month uptick, with every month successively stronger (for probably the most half) than seasonally typical for the spring into summer time buying season. July’s month-to-month stock carry at 5.1%, for instance, dwarfs the 1% common for July throughout 2018 and 2019.

Whereas the pool of stock is rising shortly, a extra substantial improve in for-sale listings has been hindered by slowing new development – residence begins fell 9.6% in July from June – and normal hesitation from would-be sellers. New for-sale listings of present properties fell 13.6% month over month in July. A far greater drop than is seasonally typical, the speed of recent listings hitting the market has been slower than pre-pandemic norms for the reason that starting of the 12 months. In July for instance, 16.6% fewer new listings had been put available on the market than the common July from 2018 and 2019. Would-be sellers stay conscious of their capacity (or lack thereof) to buy their subsequent residence and rising mortgage charges have left many owners “locked in” to their present rate of interest. An enormous wave of householders refinanced through the pandemic, both to learn from traditionally low mortgage charges immediately or to reap their residence’s fairness with a money out refinance. Low-cost financing supplied a chance for a lot of to transform their property to raised meet their altering wants fairly than transfer on. Consequently, the latest will increase in for-sale stock are extra reflective of lowered competitors than any actual improve within the general choices that patrons could have over their multi-month buying expertise. What’s extra, this lack of recent itemizing exercise ought to proceed to buoy residence costs towards persistent or deeper declines.

Energetic sellers and their brokers are immediately having to regulate to the altering market situations. The share of for-sale listings with a value minimize jumped to 18.6% in July – up 7.5 share factors from July 2021 and greater than double the share of listings that noticed a value lower in April. Whereas the general share of listings seeing a value discount isn’t irregular – within the years previous the pandemic it wasn’t unusual for one in 5 listings to regulate their value through the month to assist the property promote in affordable time – the sharp improve on this exercise is a loud indicator of how sellers are shifting their pricing methods to account for shortly altering market situations, even when latest value reductions haven’t materialized into true bargains for residence customers but.

Hire development continues to average

The rental market stays in a interval of relative calm, persevering with a pattern that’s shaped in latest months. The nation’s typical month-to-month lease in July was $2,031, up 0.6% from June and up 13.7% from a 12 months prior. After a fast run-up that peaked in February, and seeing increased volatility all through the pandemic’s first 12 months and a half, lease development has moderated in latest months. That mentioned, though development is decelerating, the annual development charge remains to be greater than thrice that of July 2019.

Amongst main metros, probably the most vital slowdowns in month-to-month lease development since July of final 12 months occurred in Las Vegas (from 3.6% to -0.2%), Phoenix (3.5% to -0.3%), Tampa (3.9% to 0.3%), and Austin (3.8% to 0.7%).

The Huge Image

The housing market is in the end correcting for excessive strain through the pandemic. Nonetheless, challenges to new provide and powerful long-run housing demand pushed by large youthful generations growing older into first-time residence shopping for means that, because the slowdown continues to progress and competitors and value pressures ease, sufficient patrons can be prepared to maneuver ahead and switch the market again towards (hopefully more healthy) optimistic value development.