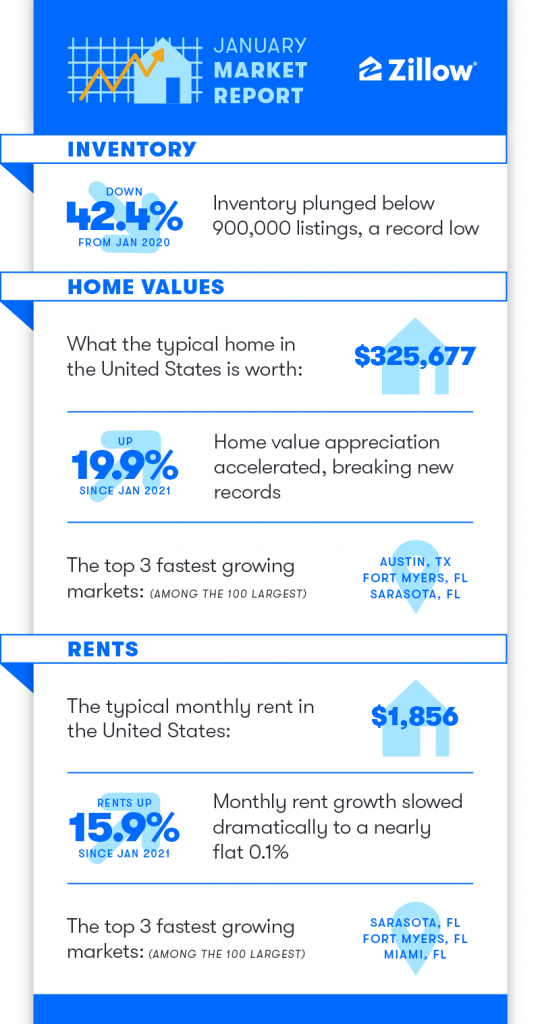

- Residence worth appreciation accelerated once more in January, to a file 19.9% annual achieve.

- Stock plunged beneath 900,000 listings, a file low – down 42.4% from January 2020.

- Annual lease development of 15.9% was down barely from earlier peaks, and month-to-month development was primarily flat.

Patrons are prone to face one other difficult house buying season later this 12 months, contending with record-low stock and unprecedented worth development. But when early-bird patrons out there within the early months of the 12 months had been deterred by rising mortgage charges and costs, their absence didn’t register: Residence worth appreciation accelerated once more, possible due to the record-low variety of listings on provide.

The Zillow Residence Worth Index (ZHVI) rose 1.5% in January from December, to $325,677, up 19.9% from January 2021. The annual development price represents an all-time excessive in knowledge courting again greater than 20 years – and the month-to-month tempo continued its re-acceleration since November’s latest low of 1.2%. If month-to-month worth development had been to carry regular at January’s tempo, that may translate to an annual development price of 19%, or virtually equal to the present year-over-year achieve.

The midwinter market warmth was widespread throughout native markets. Month-to-month house worth development accelerated from December to January in 38 of the nation’s 50 largest metropolitan areas. Among the many nation’s 50 largest markets, the slowest month-to-month development in December was in Milwaukee (0.7%), adopted by New York (0.7%) and Washington, DC (0.7%). The quickest was in Nashville (2.5%), San Diego (2.5%) and Las Vegas (2.5%).

Stock Plunges to File Lows

After December’s bone-dry stock drought, house customers could have been waiting for January for listings to be replenished. However house sellers evidently didn’t get the memo. Energetic stock dropped 13% from January – the 2nd straight double-digit month-to-month drop and the most important month-to-month decline in at the very least three years. That left energetic stock 22% decrease than a 12 months in the past, and 42.4% decrease than January 2020 – the eve of the pandemic outbreak.

The proximate explanation for the shortfall was a pointy cutback within the stream of recent listings hitting the market, which slackened by 19% from December’s price of recent listings. That additionally places January’s stream of recent listings beneath its two-year comparability month’s price, for the primary time since July, when month-to-month worth appreciation peaked. That means that market circumstances are solely getting more durable for patrons, at the very least in the meanwhile.

Stock was down in January from December in at the very least 49 of the nation’s 50 largest metros (month-to-month knowledge for Nashville is unavailable), and was down year-over-year in 47 of the 48 largest metros for which full knowledge is accessible (January 2021 knowledge for Milwaukee and Nashville is unavailable). The biggest annual stock declines in January among the many largest 50 markets had been in Miami (-49.9%), Sacramento (-38.1%), and Denver (-37.7%). Stock was up year-over-year in Austin (+18.7%).

Much like December, if there may be one small silver lining for frenzied would-be homebuyers contending with speedy house worth appreciation and restricted stock, it’s that the pace of the market has regularly slowed down since reaching a peak early final summer time – and seems to have stabilized for now. In June, the everyday U.S. house spent only one week available on the market earlier than going below settlement. That timeframe rose to roughly 13 days in December and January. It’s value noting that properties sometimes take longer to promote within the fall and winter months as back-to-school, shorter days and the vacation season all are likely to eat into each patrons’ and sellers’ schedules. However whereas properties staying available on the market lower than two weeks earlier than promoting remains to be extremely quick for midwinter, these further few days could matter lots to these patrons that want somewhat extra time to evaluate their choices.

Even so, the fact of the state of affairs on the bottom is difficult to disregard. Residence patrons immediately are making bids and shutting offers regardless of a few of the most difficult circumstances ever: record-few properties on the market to select from, priced at double-digit good points from final 12 months, financed at sharply rising mortgage charges. It stays to be seen how lengthy patrons can climate this storm, and the way lengthy householders will watch values rise earlier than deciding to record. This month’s knowledge inform us neither have blinked but. Anticipate a scorching scorching spring buying season.

Peak lease development?

The Zillow Noticed Hire Index rose 15.9% year-over-year in January, to $1,856/month. However month-to-month lease appreciation plunged to 0.1%, as rents fairly practically flatlined. Meaning renters who signed 12-month leases final winter are possible in for some sticker shock on their renewal presents, however anybody who’s been looking leases earlier within the winter received’t see a lot of an uptick in comparison with final month.

Rents grew year-over-year in all 50 of the nation’s largest metros. Among the many 50 largest metros, annual lease appreciation was quickest throughout the Sunbelt, with the quickest development in Miami (30.6%), Tampa (28.2%), Phoenix (25.6%) and Las Vegas (24.8%). Annual lease development was slowest in Minneapolis (5.9%), Pittsburgh (7.8%) and Milwaukee (8.1%).

The speedy development in rents is now being picked up, after a delay earlier this 12 months, in official measures of inflation. The primary Client Value Index part measuring rents, the Hire of Main Residence, rose 3.8% year-over-year in January, or simply over 0.5% month-over-month. Mixed with rising House owners’ Equal Hire, which was up 0.4% in January, the rising shelter parts of the CPI are contributing to total inflation – now registering its quickest development in virtually 40 years.

Trying Forward

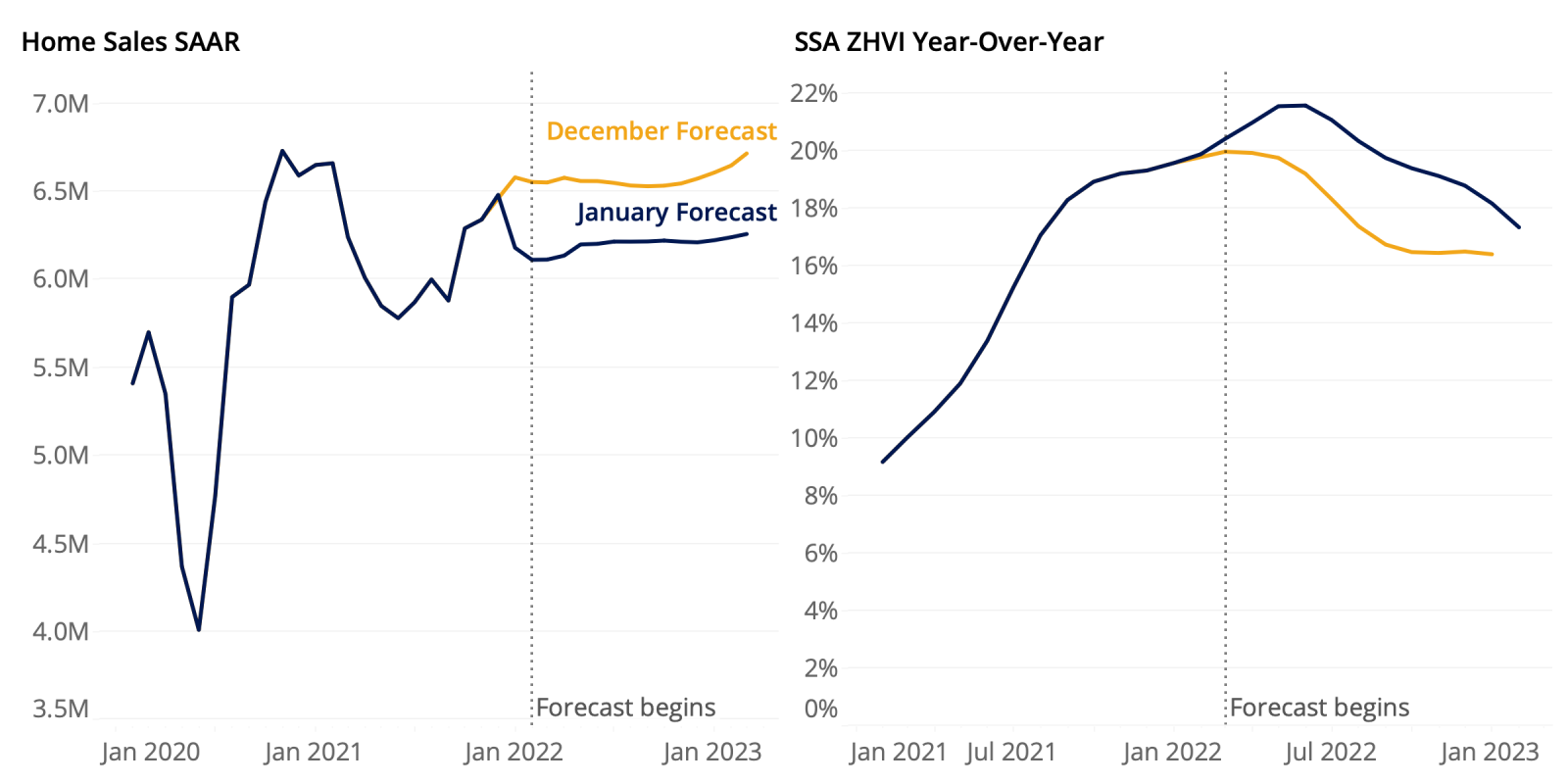

Annual house worth development is projected to proceed accelerating via the spring earlier than peaking at 21.6% in Might, earlier than regularly slowing via January 2023. Greater than 6.2 million complete current properties are anticipated to promote in 2022.

Month-to-month house worth development can be anticipated to proceed accelerating in coming months, rising to 1.7% in February and rising to 1.9% in April earlier than slowing considerably. By the top of January 2023, the everyday U.S. house is predicted to be value greater than $380,000. The strong long-term outlook is pushed by our expectations for tight market circumstances to persist, with demand for housing exceeding the provision of accessible properties.

The seasonally adjusted annual price of current house gross sales in January is predicted to complete greater than 6.11 million, down 1.1% from December and eight.1% from January 2021 (January 2022 current house gross sales knowledge are scheduled to be launched by the Nationwide Affiliation of Realtors on Feb. 18, 2022). Current gross sales quantity (SAAR) is predicted to develop all through the spring house buying season, earlier than falling very barely starting in July. General, Zillow expects greater than 6.2 million current properties to promote in 2022, up 1.6% from an already robust 2021.

The seasonally adjusted annual price of current house gross sales in January is predicted to complete greater than 6.11 million, down 1.1% from December and eight.1% from January 2021 (January 2022 current house gross sales knowledge are scheduled to be launched by the Nationwide Affiliation of Realtors on Feb. 18, 2022). Current gross sales quantity (SAAR) is predicted to develop all through the spring house buying season, earlier than falling very barely starting in July. General, Zillow expects greater than 6.2 million current properties to promote in 2022, up 1.6% from an already robust 2021.

Nevertheless, draw back dangers to our forecast stay. Quickly rising mortgage charges current a significant headwind to housing demand, significantly in costlier markets.