naveen0301/iStock Unreleased by way of Getty Photos

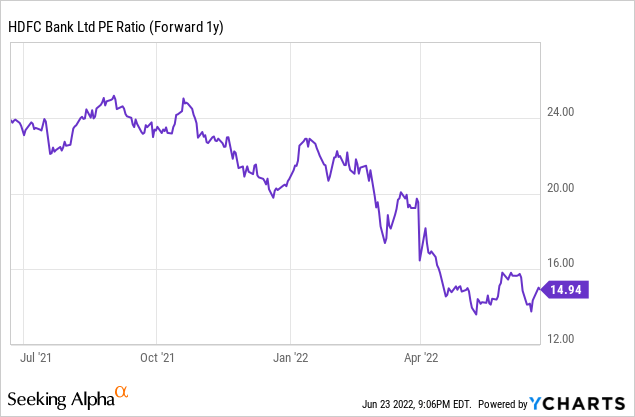

HDFC Financial institution Restricted (NYSE:HDB) is coming into a brand new chapter in its development story with the HDFC merger. Publish-transaction, the financial institution will see accelerated steadiness sheet development, permitting it to ramp up investments in capability-building throughout its folks, bodily and digital channels. Essentially the most distinguished strategic shift will doubtless be within the mortgage development runway, which is able to obtain a serious enhance publish the merger of HDFC Restricted into the financial institution. Whereas near-term merger uncertainties may weigh on earnings, this appears to be largely priced in on the present valuation low cost relative to historic ranges (~15x fwd earnings). This supplies a compelling entry level for affected person, long-term buyers to appreciate the long-run RoE accretion as value advantages kick in post-merger.

Urgent the Retail Progress Pedal Publish-COVID

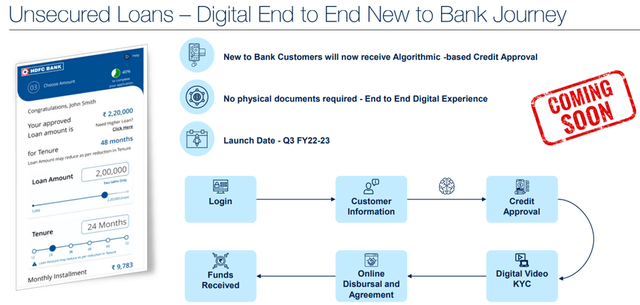

HDB’s commentary on the latest investor day and earnings name had been equally optimistic, emphasizing the pick-up in retail phase development throughout product strains popping out of the pandemic (recall that the financial institution had beforehand pulled again on retail loans throughout COVID). As the largest GDP contributor and a supply of energy for HDB by means of the years, the deal with housing is smart, with HDB planning to develop the house mortgage guide aggressively to make up for misplaced floor. As well as, HDB may also leverage its superior worth proposition in auto and unsecured mortgage classes (e.g., bank cards and private loans), the place it presently holds the main market share. HDB cited gold loans as a possible development space as nicely, with plans to triple or quadruple the department rely providing this product. Progressive choices such because the ten-second private mortgage product are additionally being rolled out to new-to-bank prospects, probably increasing its universe of addressable market alternatives going ahead.

HDFC Financial institution

Strong Company Progress Numbers to Proceed

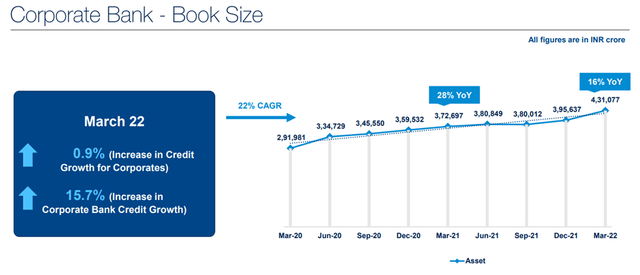

To make up for the retail phase slowdown throughout the pandemic, HDB has opportunistically leaned on asset development in its company enterprise. The energy right here was led by a formidable ~16% development in company loans in FY22 (vs. ~1% for the system) on expectations of a broader capex revival. Supported by authorities expenditure, public sector capex ought to do nicely, whereas the deal with non-public sector capex is smart given the necessity for provide chain finance amid the continuing disruptions. The financial institution is much less occupied with taking part in lending by way of company bonds, although, which ought to imply its best-in-class value ratios and credit score prices stay intact. As a substitute, HDB will transfer deeper into the multinational firms (MNC) sector within the coming years – though MNCs signify a comparatively smaller addressable market alternative, the outsized charge and foreign exchange earnings technology may very well be a pleasant earnings tailwind.

HDFC Financial institution

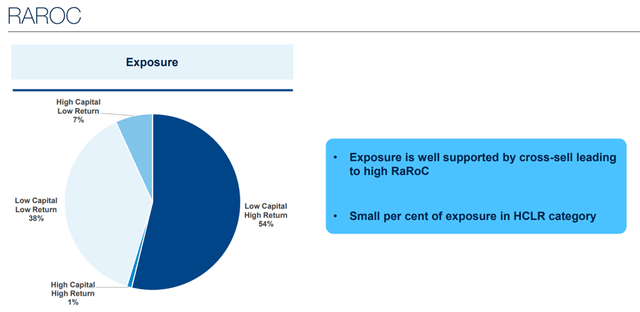

The overarching takeaway from HDB’s company presentation, for my part, is its continued deal with sustaining industry-leading company risk-adjusted return on capital (RAROC). Initiatives right here ought to hold the ROA profile wholesome, even with out the advantages of cross-selling from different lending merchandise. Asset high quality doubtless stays pristine as nicely, with ~54% of the portfolio within the “low capital, excessive return” bucket and ~87% rated AA/above. Plus, HDB has ample room to maneuver for higher yields with out compromising its RAROC mannequin, given the financial institution remains to be under-penetrated amongst corporates – it has but to ascertain a relationship with 617 corporates (income of >INR10bn) inside its eligibility standards, equating to a mixed INR11tn debt measurement.

HDFC Financial institution

Close to-Time period Merger Uncertainties Outweighed by Favorable Lengthy-Time period Economics

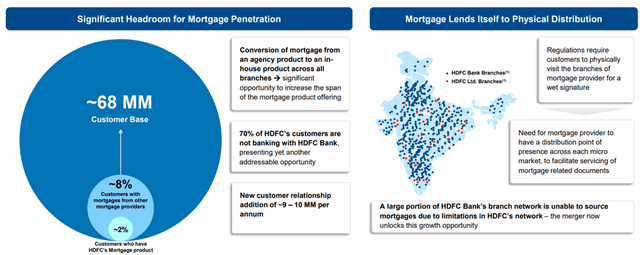

To this point, HDB inventory seems to have priced within the margin and profitability overhang from the pending HDFC-HDFC Financial institution merger. Whereas the near-term considerations are legitimate, the long-term economics from this deal appear overwhelmingly optimistic, given the advantages from a decrease funding value to the mortgage guide in addition to different post-merger synergies, together with cross-selling alternatives. The latter is essential – lower than 2% of the HDB buyer base has a house mortgage from HDFC, and ~5% have taken a house mortgage from one other lender, so penetration right here may considerably prolong the expansion runway. Plus, the outlook for Indian housing is bullish, and by harnessing HDFC’s experience, HDB can be higher positioned to capitalize on future alternatives.

HDFC Financial institution

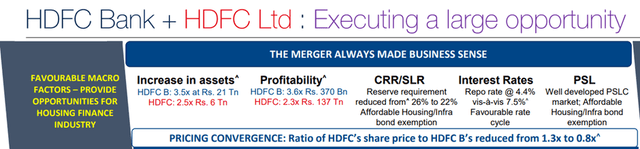

Within the meantime, numerous merger-related considerations stay high of thoughts. Specifically, managing regulatory prices within the type of the Money Reserve Ratio (CRR) and the Statutory Liquidity Ratio (SLR) reserve upkeep can be key to making sure a ROA/ROE accretive end result. The surplus liquidity buffer of HDFC and HDB ought to assist, although, whereas the price of precedence sector lending certificates (PSLC) purchases is guided to have a manageable 5-10bps near-term drag on the RoA. Given regulatory approval phrases, the proposed construction may also doubtless be a comparatively easy HDFC + HDFC Financial institution merger (versus a Non-operative Monetary Holding Firm (NOHFC) construction). This suggests a desire to carry a >50% stake in its subsidiaries, though there’s flexibility right here given administration’s consolation in holding <30% relying on regulatory necessities. Nonetheless, the merger base case stays for the transaction to be guide worth accretive and ROA impartial/optimistic within the mid-term, though ROEs are projected to take three to 5 years to revert to bank-level. HDB administration’s execution monitor document has been pristine to this point, so I really feel comfy underwriting the case for an accretive post-merger end result over the long term.

HDFC Financial institution

Finest-in-Class Indian Financial institution Weighed Down by Transitory Headwinds

Total, I see HDB (pre-and post-merger) as providing best-in-class asset high quality throughout the Indian banking sector. Working example – the financial institution delivered sector-leading profitability by means of the cycles (even throughout the demonetization interval in 2016 and COVID in 2020), a monitor document no different Indian financial institution can match. With robust buyer acquisition and ample cross-selling alternatives (post-merger) to its large buyer base additionally set to drive extra market share positive factors, the HDB future seems brilliant. Valuation-wise, HDB has suffered a de-rating since I final coated the inventory and now trades at a reduction relative to historic ranges amid the merger-related uncertainty. This presents a possibility to long-term buyers, for my part, as income and margins look set for continued development into the approaching years, whereas additional readability on the HDFC merger ought to ease the overhang within the months forward.