- Month-to-month funds on a typical mortgage are greater than 75% larger than they had been in June 2019.

- Affordability challenges are tamping down competitors in previously red-hot markets, inflicting steep drops in pending gross sales in locations like San Jose, Seattle, and Salt Lake.

- Typical U.S. rents have surpassed $2,000 a month for the primary time, however progress is easing.

House consumers are fewer and farther between than they’ve been for a lot of the pandemic. At this time’s consumers are going through robust affordability headwinds, however those that can, or should, nonetheless purchase, are beginning to profit from a extra balanced market in comparison with the pandemic-fueled rush on actual property in 2021. They’ve extra choices to tour, extra time to search out the precise home, and are much less more likely to face a bidding battle.

Regardless of this preliminary transfer towards rebalancing, the market continues to be much less buyer-friendly than the pre-pandemic norm in many of the nation. The month-to-month mortgage cost on a typical U.S. house grew one other 4.5% in June, and is now 62.3% larger than it was a yr in the past and 75.7% larger than in June 2019. [1]

Value progress cooldown continues

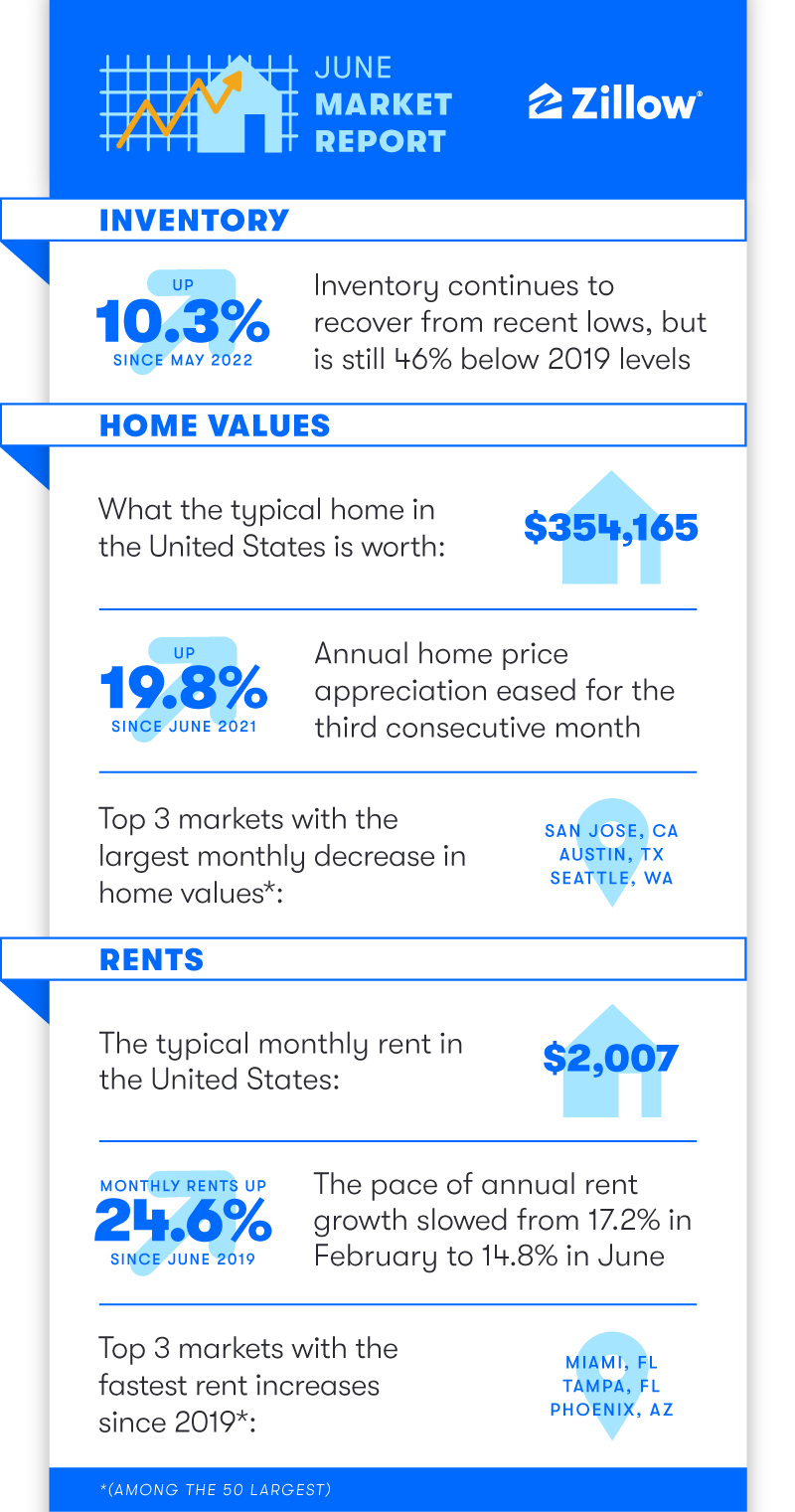

Affordability obstacles are the seemingly main trigger for decelerating house worth progress. Annual house worth appreciation cooled for the third consecutive month in June, stepping right down to 19.8% from a report excessive of 20.9% in April. However it nonetheless towers over the 4.6% year-over-year progress recorded in June 2019, earlier than the pandemic. The everyday U.S. house worth now stands at $354,165, in line with the Zillow House Worth Index.

Month-to-month value progress has slowed sharply, down from 1.6% in April to 1.2% in June (smoothed, seasonally-adjusted). Even decrease uncooked month-to-month value progress of 0.8% suggests additional deceleration within the close to future.

House values truly declined barely from Might to June in San Jose, Seattle, San Francisco and San Diego — all among the many 5 most costly main metro areas — in addition to in Austin, the place house values have grown essentially the most all through the pandemic. Annual appreciation continues to be strong in these metros — from 15.4% in San Francisco to 25.2% in Austin. However a pointy rise in stock and excessive charges of itemizing value cuts all level to a marked cooldown in these top-flight markets for a minimum of the subsequent few months.

Choosy consumers are leaving extra stock on the shelf

Stock has risen steadily this yr, bringing a year-over-year deficit of 30.4% in January right down to 9.1% in June. However the complete pandemic gap is much from being stuffed — stock continues to be down 46% since June 2019.

Extraordinarily costly metros and people with the biggest run-up in costs over the course of the pandemic — San Francisco, Austin, Phoenix and Seattle — have stock ranges closest to the place they had been in 2019. That is one other indication that competitors in these areas is easing up extra rapidly than elsewhere within the U.S.

An absence of inexpensive choices is driving a slowdown in gross sales, as properly. Of the 15 main metros that noticed the biggest month-over-month drops in newly pending gross sales, 12 are among the many nation’s 15 most costly housing markets. The quickest drops in newly pending gross sales from Might to June occurred in San Jose (-24.3%), Seattle (-23.9%) and Salt Lake Metropolis (-20.8%).

Conversely, of the 15 main metros with the smallest month-to-month pullback in gross sales, 10 are among the many 15 least-expensive giant markets.

Median time available on the market has ticked up, that means consumers have barely extra time to buy, evaluate and consider choices. Listings that go pending are sometimes doing so after seven days, which suggests competitively priced houses are nonetheless promoting at a speedy clip.

The share of houses with a value reduce can be rising throughout the U.S., and at 14.8% is on the highest degree since November 2019. Salt Lake Metropolis (24.1%), Sacramento (21.7%) and Phoenix (20.4%) are seeing the best shares of listings with value cuts.

Rental market normalizing

Typical U.S. rents rose 0.8% from Might and at the moment are $2,007 monthly, crossing the $2,000 threshold for the primary time. Annual hire progress has eased steadily from a record-high 17.2% in February to 14.8% in June. Rents are up 24.6%, practically $400 monthly, since June 2019.

The speedy hire progress that peaked in February was seemingly a one-time occasion, pushed by a return to cities and other people transferring out of shared residences or their mother and father’ home. However the excessive value of shopping for a house might even see rents reverse course within the coming months as renters choose to resume their leases or search for one other rental fairly than wade into the costly for-sale market.

Florida nonetheless tops the hire progress leaderboard, with rents rising the quickest yearly in Miami (28.3%), Orlando (22.4%), and Tampa (22.2%) of all main metros. The New York metro space is simply behind at 20.5% year-over-year progress, with San Diego (+19.3%) rounding out the highest 5. The slowest yr over yr progress is discovered within the Midwest and Rust Belt: Minneapolis (6.1%), Milwaukee (7.7%), and Pittsburgh (8.4%).

Trying ahead

Zillow’s house worth forecast predicts the slowdown in annual house worth progress will proceed from the present tempo of 19.8% to 7.8% progress within the coming yr, ending June 2023. Zillow’s earlier forecast referred to as for 9.7% house worth progress within the yr ending Might 2023.

Zillow now expects 5.46 million current house gross sales in 2022. That might mark a ten.8% lower from a powerful 2021.

[1] Assuming a brand new mortgage on a typical house in line with the Zillow House Worth Index as of June ($354,165), utilizing a 20% down cost and the typical 30-year fixed-rate mortgage in June (5.52%). Principal and curiosity solely.