Mrinal Pal/iStock Editorial through Getty Photos

ICICI Financial institution (NYSE:IBN), India’s second-largest financial institution, once more delivered a powerful set of quarterly outcomes, led by a +22% YoY core pre-provision working revenue (PPOP) development on continued momentum throughout mortgage development and internet payment earnings. The ~Rs4bn internet slippage was one other key spotlight, reflecting favorable normalized credit score price developments. With its asset high quality intact and the visibility of earnings development set to enhance going ahead, I see a transparent path to the financial institution sustaining robust ROEs within the coming years. As ICICI leverages its intensive distribution franchise and best-in-class digital infrastructure to additional prolong its development runway amid an bettering post-COVID backdrop as properly, the valuation hole relative to key peer Kotak Mahindra ought to slim.

| 2023e P/E | 2024e P/E | |

| ICICI Financial institution | 19.7x | 16.9x |

| Kotak Financial institution | 27.0x | 23.2x |

Supply: Market Information as of third August 2022

Core Working Metrics Outpace Expectations

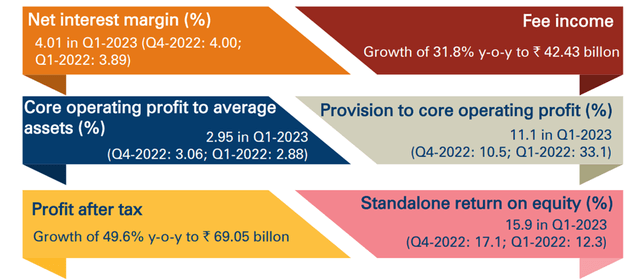

ICICI reported a robust quarter but once more, led by internet curiosity earnings development of ~21% YoY and even stronger internet payment earnings development of ~32% YoY. Though this was partially offset by larger working bills, margins nonetheless expanded at a wholesome ~9bps tempo on a sequential foundation. For context, the elevated opex was pushed by a ~20% YoY improve in worker expense – given this was largely because of the firm passing by way of the honest worth affect of its inventory choices, although, I view this as a one-off affect. In the meantime, the cost-income ratio (ex-treasury) was a strong ~42% – up by ~140bps sequentially, however properly beneath pre-COVID ranges of ~45%. Consequently, PPOP was up ~19% YoY, outpacing HDFC Financial institution’s ~15% YoY development throughout the corresponding interval. Assuming the cost-income ratio sustains at 41-42%, count on working leverage to stay excessive, benefiting the mid-term PPOP development runway.

ICICI Financial institution

Primarily based on the robust Q1 2023 outcome, the near-term trade outlook appears to be like vibrant – this quarter’s strong margin enlargement displays the advance seen at Kotak Financial institution, regardless of the yield advantage of charge hikes but to completely move by way of to the P&L. Given ICICI has top-of-the-line deposit franchises in India in addition to the next floating charge composition inside its portfolio, the financial institution is well-positioned to drive margins even larger. Having additionally delivered a ~20% PPOP CAGR in recent times, I see no purpose why ICICI will not have the ability to ship a high-teens % core PPOP by way of 2025 in a base case state of affairs. The important thing right here would be the extent of the approaching repo charge hikes and administration’s capability to handle any aggressive pressures in mortgages and different shopper retail merchandise.

Spectacular Development Momentum Continues in Lending Enterprise

ICICI’s home mortgage development is clearly heading in the right direction – mortgages had been up 22% YoY, whereas share positive aspects in SMEs/enterprise banking led to ~35% YoY positive aspects. Accelerating development in unsecured credit score at 40-60% YoY contributed to the rest of the YoY development, driving a sturdy ~32% YoY core payment development. Extra importantly, ICICI has achieved this development with out compromising on its mortgage guide composition – the financial institution has gained share in playing cards and mortgages, however its market share stays comparatively low within the SMEs, rural and company sectors at 4%-5%. General, advances had been up ~21% YoY this quarter (one other consecutive quarter of robust mortgage development), though the sequential mortgage development of 4.3% QoQ was significantly spectacular given it was the very best for a Q1 because the 2013 fiscal yr. The outlook for loans appears to be like vibrant as properly – the economic system is opening up post-COVID, which suggests ICICI ought to profit from an enchancment in revolvers, together with potential untapped development alternatives from Manufacturing Linked Incentive (PLI) schemes.

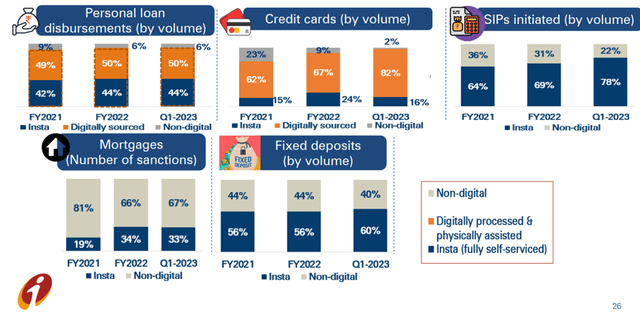

One other key spotlight from ICICI’s outcome was the rising traction in digital channels, serving to to amplify the tempo of disbursements – per administration, digital contributed ~94% of non-public mortgage disbursements, ~98% of bank cards sourcing, and ~33% of mortgage loans. The digital issue might be key at a time when HDFC Financial institution is getting more and more aggressive publish lifting of the RBI ban on new issuance of playing cards. To this point, ICICI has doubtless misplaced some market share YTD, significantly in bank card spending, however with its robust digital capabilities, ICICI retains the potential to regain market share and outperform on mortgage development over the mid-term.

ICICI Financial institution

Asset High quality Enchancment Helps Double-Digit ROE Outlook

Gross non-performing loans (GNPLs) are trending favorably as properly, reaching 3.6% of loans (down ~20bps sequentially) on robust ~16% restoration charges (of opening GNPLs) – for comparability, ICICI has usually seen GNPLs pattern between 10% and 13% in current quarters. The non-NPL confused portfolio additionally improved by ~50 bps to 2.2% of loans, helped by a discount within the restructured portfolio in addition to enhancements within the sub-BB guide. No shock then that internet slippage additionally outpaced expectations at ~Rs4bn regardless of elevated agriculture stress, driving the general core credit score price to near-zero ranges.

ICICI Financial institution

In the meantime, ~Rs11bn has been added to the contingency fund (now ~1% of loans), bringing the general provision protection ratio on confused/restructured loans larger to 74.3% (up by ~640bps). This implies ICICI’s provision protection is catching up with HDFC Financial institution (HDB), regardless of its larger secured combine – for context, HDB additionally noticed its protection ratio rise ~670bps to 84% throughout the corresponding interval. In flip, this affords ICICI extra flexibility heading into potential macro turbulence, supporting its mid-term ROE sustainability and high-teens % core PPOP development runway.

Lengthy-Time period Compounding Potential Intact

With one other robust quarter within the bag, that includes outperformance on NIMs and core PPOP development on the again of an bettering internet curiosity/payment earnings outlook, ICICI appears to be like set to increase its lead throughout the Indian banking trade. The financial institution has additionally seen power in its asset high quality (according to the sector), emphasizing that any COVID overhang is probably going behind us. Thus, the trail to near-term upside will doubtless relaxation on NIMs and Present Account/Saving Account (CASA) developments, putting ICICI in pole place given its best-in-class deposit franchise in a rising charge backdrop. Valuation-wise, the inventory presents compelling worth on the present low cost to see Kotak, significantly given ICICI’s materials development and profitability enchancment relative to historic ranges.