Matthew Speakman is a senior economist at Zillow. He shared his ideas about what’s driving the latest spike in mortgage charges, how that can influence the broader housing market, and the place the market will go from right here.

What’s inflicting this fast rise in charges?

Numerous elements have pushed mortgage charges firmly increased this 12 months, however inflationary pressures are the principle offender.

All else being equal, inflation locations upward stress on bond yields, which usually dictate the trail of mortgage charges. Inflation is operating at a 40-year excessive and mortgage charges have, by some measures, seen the best annual progress because the late Nineteen Seventies. Evidently, traders are eagerly looking for indicators that inflation is cooling. Hints of calming value progress in Could led mortgage charges to briefly plateau. However Could’s official inflation information got here in hotter than anticipated, prompting a tremendously sturdy surge increased for mortgage charges within the days that adopted.

Mortgage charges additionally replicate markets’ expectations for the way the Federal Reserve goes to tighten financial coverage with a purpose to rein in rising costs. Considerably confusingly, the Fed’s actions are literally much less influential on mortgage charges than the market’s expectations for what the central financial institution goes to do going ahead. Fears that the hotter-than-expected Could inflation information would lead the Fed to make a way more aggressive coverage determination helped affect the fast hike in mortgage charges in mid-June. The financial institution’s precise determination to extend in a single day charges by 75 bps really resulted in a decline in mortgage charges.

Whereas mortgage charges stay very excessive in comparison with latest years, they’ve come down a bit because the frenzy of mid-June. Inflationary pressures are displaying few indicators of abating, however the Fed’s insistence that it’s “strongly dedicated” to curbing inflation has triggered some traders to melt their progress outlook for the years forward. This alteration in tune has launched some downward stress on bond yields and, thus, mortgage charges in latest days.

What do you assume will occur to charges sooner or later?

It’s at all times extraordinarily troublesome to foretell mortgage fee actions, notably at a time with such financial and geopolitical uncertainty like there’s immediately. For instance, there’s been a basic perception mortgage charges would rise this 12 months, however few may have predicted what has performed out over the previous couple of weeks – each the surge increased in mid-June and the pullback of charges in latest days.

As I discussed earlier, considerations about persistent inflation will proceed to have a robust affect on mortgage charges till there’s ample proof that value progress is easing. The pandemic and geopolitical developments are additionally inputs into this calculus. Issues in regards to the financial system’s longer-term progress prospects, and the potential of a recession within the near-future, are additionally factoring into the market’s outlook for bond yields, which usually affect mortgage charges.

What influence may this have on the housing market?

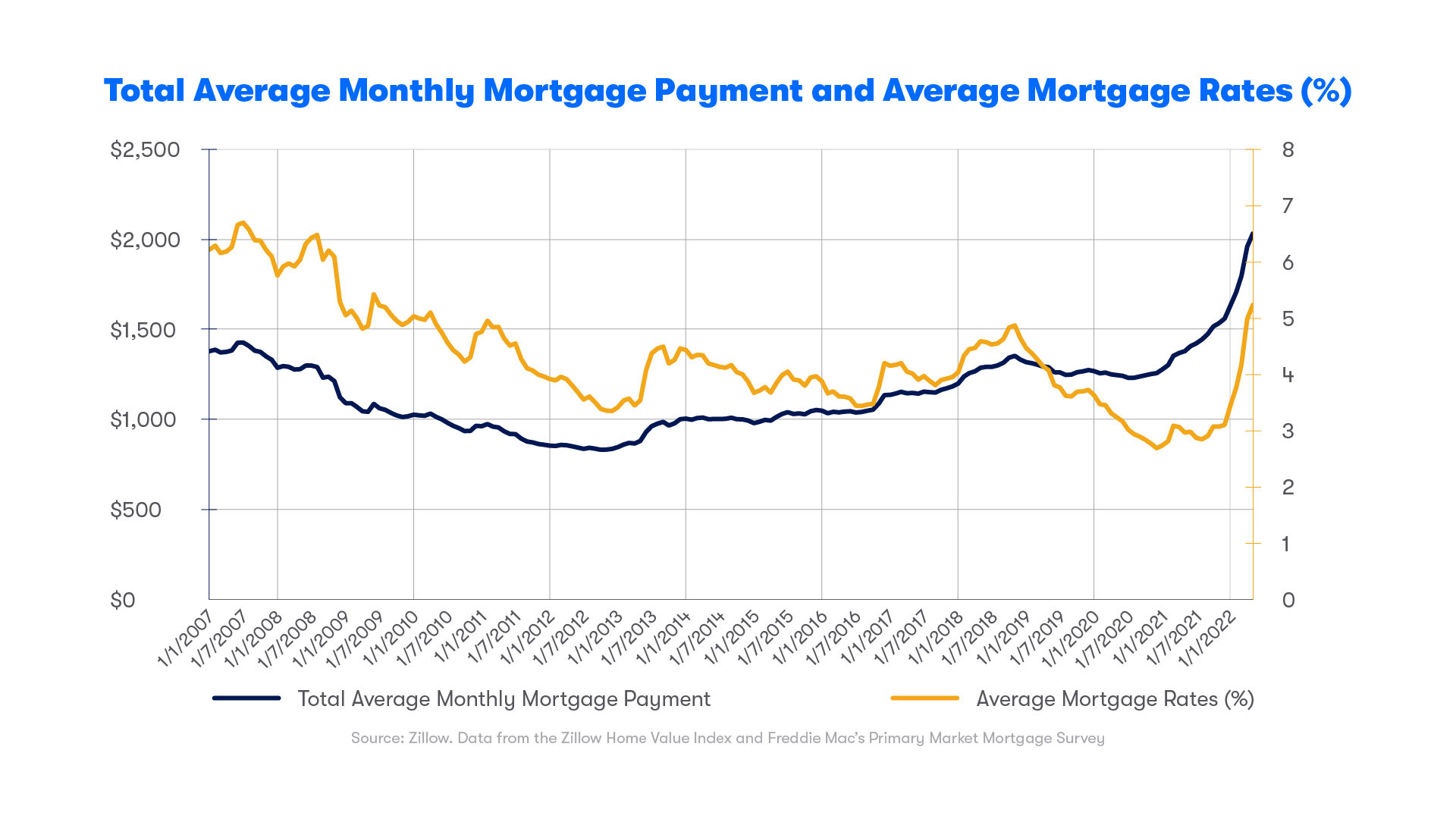

Greater mortgage prices ought to calm demand and usher in some much-needed rebalancing of the market. The mix of the latest record-breaking tempo of house worth progress and immediately excessive mortgage charges has severely worsened housing affordability. Our affordability measure exhibits {that a} month-to-month mortgage cost on the nation’s typical house makes up a larger share of median home-owner earnings than at any time since at the very least 2007, and probably for much longer. These worsening circumstances are already having an influence available on the market – house value progress has began to melt and value cuts have gotten extra frequent, as sellers are lastly being challenged and start to rethink their expectations.

Mortgage charges’ rise pushes month-to-month funds skyward

Whereas they continue to be low by historic requirements, for-sale stock ranges have risen. A slower tempo of gross sales has resulted in additional houses staying available on the market for longer. New itemizing exercise continues to lag behind latest years.

It’s vital to do not forget that whereas mortgage charges are definitely not the one purpose why householders determine to maneuver, they do issue into the equation, and for some potential movers, the prospect of giving up their present mortgage and taking up one with a fee that’s practically double their present one is sufficient to again out of the transaction.

What would occur if charges went again down?

A pointy discount in mortgage charges would naturally reenergize exercise within the housing market, and incentivize some consumers and sellers who’re presently on the fence to leap again into the market. Total affordability challenges would persist as costs stay excessive, however it’s doubtless that many potential consumers – notably these first time consumers who’ve confronted a very aggressive market over the previous couple years – would view decrease charges as a chance to lastly enter the market. On the vendor’s aspect, those that are involved about having to tackle a better fee in the event that they have been to surrender their present one would after all be confronted with an easier-to-digest situation.