- Stock fell in February, breaking with previous yearly tendencies, and now stands 48% under February 2020.

- Residence worth appreciation has accelerated to begin the 12 months, and the everyday U.S. house was price 32.4% extra in February than in February 2020.

- Hire costs reversed a cooling pattern; a one-year lease now would price almost $3,400 multiple signed two years in the past.

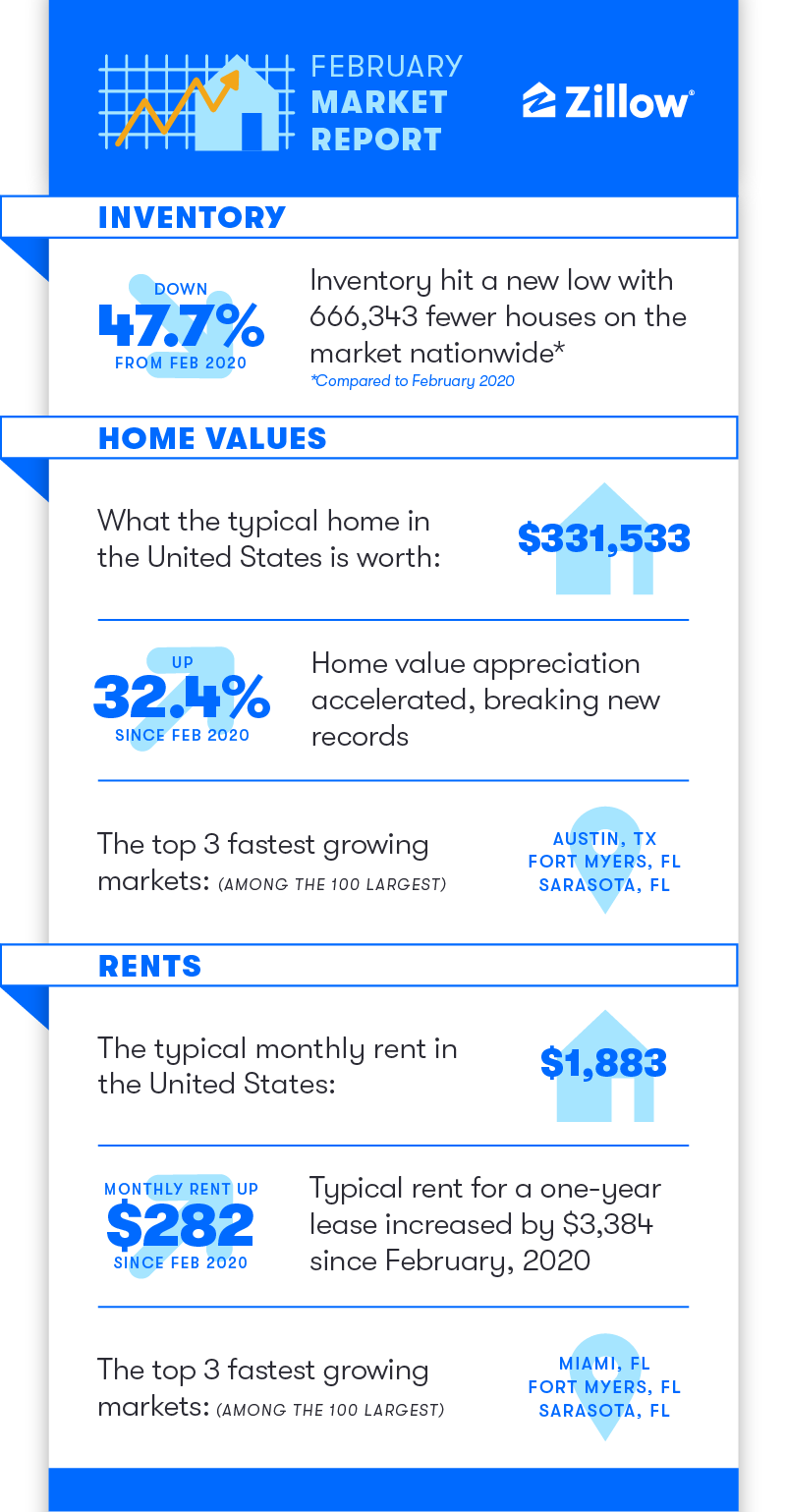

The variety of properties on the market in February was down by virtually half from the fast pre-pandemic interval two years in the past, serving to push housing prices up throughout the board all through the transformative, two-year pandemic period. Rents are up by a whole bunch of {dollars} per thirty days and residential values up by virtually a 3rd over the identical span, in response to the February 2022 Zillow Month-to-month Market Report.

However nonetheless, regardless of the quickly rising prices, demand from house consumers stays sturdy, with listings flying off the market and gross sales stronger than pre-pandemic ranges.

The important thing metric driving these historic hikes is stock. There have been roughly 730,000 properties on the market nationwide in February, in comparison with 1.4 million in February 2020. Traditionally, stock has typically bottomed out in December after which rebounded as sellers listed their properties in preparation for the busy spring purchasing season. However this 12 months, provide has continued to dwindle properly into the brand new 12 months and stock was 11.9% decrease in February than in January.

Of the 50 largest U.S. metros, these with the biggest stock deficit since 2020 are Raleigh (-69.7%), Hartford (-63%), Windfall (-61.8%) and Miami (-61%). These seeing the smallest lower are San Francisco (-7.8%), San Jose (-17.9%) and Austin (-26.9%).

However enduring and very robust demand from house consumers meant that these properties that had been listed acquired scooped up in simply 11 days in February, six days quicker than February 2021 and a full 25 days quicker than in February 2020.

And regardless of the difficult purchasing setting, gross sales are nonetheless brisk for this time of 12 months. Extra properties transacted final month than in both February 2019 or 2020, although gross sales had been 11% decrease than in 2021. Gross sales typically sluggish by way of March earlier than taking off in April, possible what we’re seeing now.

Residence Worth Progress: One other File-Shattering Month

Economics 101 says the online impact of restricted provide and sturdy demand is quickly rising costs. The everyday U.S. house is now price $331,533 – up 32.4%, or $81,000, from February 2020. Residence values rose 20.3% in simply the previous 12 months alone, one other new file for annual appreciation. In February 2020, annual house worth development was 3.7%, a determine far more according to longer-term historic norms. And the speed at which house values are rising has additionally accelerated, with month-over-month appreciation hitting 1.6% in February, up from a current low of 1.2% in November.

All 50 of the nation’s largest metro markets skilled double-digit year-over-year development in February. Annual development was quickest in Austin (45.4%), Raleigh (33.1%) and Tampa (31.%); annual development was slowest in Baltimore (11.5%), Washington, D.C. (11.6%) and Milwaukee (11.7%). On a month-to-month foundation, among the many identical 50 markets, development was quickest in Salt Lake Metropolis, Raleigh and Nashville (all at 2.6%); month-to-month development was slowest in New York (0.8%), Philadelphia (0.8%) and Chicago (0.9%).

Rental Market Not Immune

The for-sale market is the obvious place to look to see the consequences of restricted provide, however the rental market is just not immune, both. These consumers, particularly growing old millennials, trying to find a house to purchase however not discovering one which meets their wants, finances and/or location desire – or shedding out on that house to increased/quicker bidders – means they’re prone to keep renters longer. There are additionally possible many present renters that would like to personal, however usually are not but prepared or are unable to enter the market due to monetary or different concerns. On the identical time, the big Gen Z era is starting to strike out on their very own and enter the rental market as properly. Mixed, this excessive rental demand is holding rental emptiness charges close to all-time lows and pushing lease costs – after a short, early pandemic pause – up at an virtually equally quick tempo as house values.

Rents in February reversed January’s temporary cooling pattern, taking pictures up 1.1% from final month and 17% from final 12 months. Typical lease throughout the U.S. is now $1,883 per thirty days, $283 per thirty days increased than in February 2020. Hire development was sluggish in 2020 after the outbreak of the pandemic however skyrocketed in 2021. The biggest month-to-month lease hikes amongst main metros had been in Buffalo (2.3%), New Orleans (2.2%), and Miami (1.9%). Solely Las Vegas and Birmingham noticed month-to-month declines, at 0.3% and 0.2%, respectively.

The pandemic introduced with it excessive demand for properties that has pushed costs to rise at beforehand unimaginable charges. Excessive demand pushed by traditionally low rates of interest and a wave of Millennial and Child Boomer consumers depleted a housing inventory that was by no means actually replenished by new development after the glut following the Nice Recession. It’s going to take a while for stock to rise sufficient to assist curb runaway worth development, at the same time as builders are working feverishly to get new development available on the market. Quickly rising mortgage charges that will make a brand new mortgage significantly dearer than their present fee may additionally discourage some householders from promoting. However the giant sums of fairness current householders are sitting on after years of speedy house worth development would possibly assist tip the scales in favor of including new stock to the market as long-time householders contemplate cashing in as this spring house purchasing season kicks off.

Trying Forward

Annual house worth development is prone to proceed accelerating by way of the spring, peaking at 22% in Might, earlier than progressively slowing by way of February 2023. Greater than 6.4 million complete current properties are anticipated to promote in 2022.

Month-to-month house worth development can be anticipated to proceed accelerating in coming months, rising to 1.8% in March and a pair of% in each April and Might earlier than slowing considerably. By the top of February 2023, the everyday U.S. house is predicted to be price virtually $400,000. The sturdy long-term outlook is pushed by our expectations for tight market circumstances to persist, with demand for housing exceeding the availability of accessible properties.

The seasonally adjusted annual fee of current house gross sales in February is predicted to complete 6.36 million, down from 6.5 million in January 2022 however up from 6.17 million in February 2021 (February 2022 current house gross sales knowledge are scheduled to be launched by the Nationwide Affiliation of Realtors on March 18, 2022). Present gross sales quantity (SAAR) is predicted to stay the identical in March as in February, earlier than climbing barely to round 6.4 million, the place it’s forecast to stay by way of the rest of the 12 months. Total, Zillow expects 6.416 million current properties to promote in 2022, up 4.8% from an already robust 2021.

Nonetheless, draw back dangers to our forecast stay. Continued elevated inflation heightens the chance of additional financial coverage tightening, which might end in increased mortgage rates of interest and weigh on housing demand.