Peter Chronis/iStock through Getty Photographs

Danger/Reward Ranking: Optimistic

They are saying there are three guidelines in actual property: location, location, location. If this stays true, The Macerich Firm (NYSE:MAC) affords an uneven threat/reward alternative. The corporate owns arguably the best high quality portfolio within the Retail REITs business whereas buying and selling at half the valuation of its main friends with decrease high quality places. Consequently, we’re including Macerich to the dox it! record for stoxdox members.

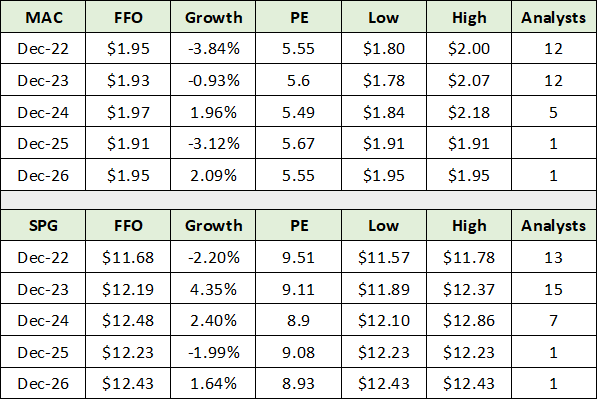

At solely 5.5x FFO (funds from operations), or money circulate within the Actual Property sector, Macerich trades at a steep low cost to Simon Property Group (SPG), which I view as a superb comparable firm. The next desk compares the valuation of Macerich to Simon primarily based on consensus FFO estimates by way of 2026. The info was compiled from Looking for Alpha.

Looking for Alpha. Created by Brian Kapp, stoxdox

Discover that the expansion estimates for every firm are the identical for all intents and functions. Each Macerich and Simon are anticipated to face stagnation over the approaching 5 years. Given the same progress profiles, the valuation distinction between the 2 have to be the results of the danger stage embedded in every firm. The market perceives Macerich to be terribly dangerous compared to Simon Property Group.

Whereas Macerich is extra leveraged than Simon, the standard of Macerich’s portfolio is decidedly greater. As we are going to see, Macerich tenants obtain materially greater gross sales on common than do Simon tenants. Consequently, the big valuation discrepancy between the 2 seems to be pricing in excessive threat for Macerich. Excluding the potential of a deep retail actual property downturn, a lot of the danger seems to be priced into the shares.

It needs to be famous that the broad Retail REITs business has been beneath appreciable stress for a while as a result of secular shift to on-line procuring. In regard to this secular stress, Macerich’s concentrate on the excessive finish of the market ought to present relative insulation compared to Simon’s. Consequently, Macerich’s high-quality belongings ought to proceed to supply help for its elevated debt ranges.

A number of Enlargement

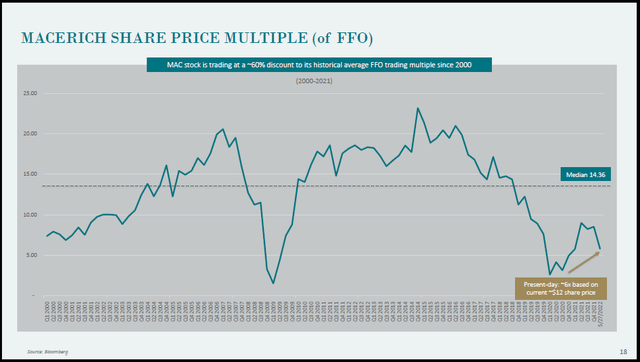

The valuation low cost hints at a valuation growth alternative for Macerich. The next slide offers additional shade on the valuation of Macerich from a historic perspective. All Macerich slides listed here are from the corporate’s June 2022 Investor Presentation.

Macerich Investor Presentation Second Quarter 2022

Whereas I do not count on Macerich to commerce at its historic median valuation close to 14x FFO, one thing extra in step with Simon Property Group’s valuation nearer to 10x FFO is an inexpensive expectation over time. Apparently, Tanger Manufacturing facility Outlet Facilities (SKT), which serves the center of the market, can also be valued close to 10x FFO in the present day.

Whereas Simon is decidedly stronger financially, the standard of Macerich’s belongings has an offsetting impact for individuals who are extra risk-tolerant. Macerich affords above-average present revenue with a 5% dividend yield and properly above-average value appreciation potential.

Location, Location, Location

Location is on the core of actual property investing. All different elements are normally subordinate within the funding choice. Whereas low-quality places can provide glorious funding alternatives if bought on the proper value, all else equal, nice places at a steep low cost are most popular.

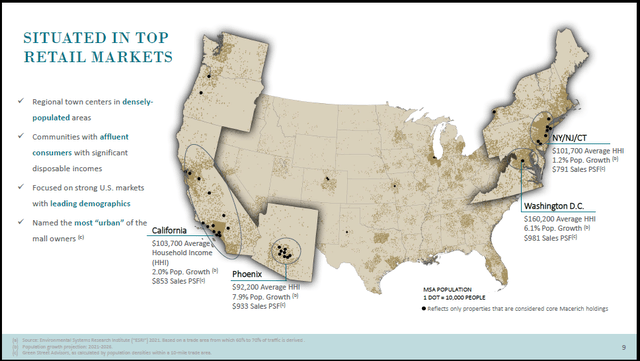

For perspective on the standard of Macerich’s portfolio, Macerich tenants are averaging retail gross sales of $843 per sq. foot whereas the final reported Simon determine was $693 in 2019. Simon now not stories this determine in its monetary releases. The next two slides show the places of Macerich’s portfolio, adopted by particulars relating to the corporate’s high ten belongings.

Macerich Investor Presentation Second Quarter 2022

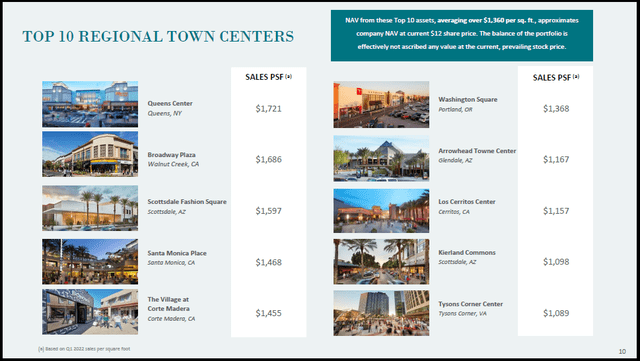

Prime Ten Belongings

Macerich Investor Presentation Second Quarter 2022

The next slide is from Simon Property Group’s Q2 2022 Supplemental Presentation. When in comparison with the Macerich property location map above, it’s clear that Simon’s portfolio is way more diversified throughout america, with broad publicity to the center market phase.

Consequently, Simon is extra uncovered to the broad retail actual property market in comparison with Macerich. By way of the secular stress mentioned above, Macerich’s concentrate on the excessive finish of the market ought to present relative insulation compared to Simon.

Simon Property Group’s Q2 2022 Supplemental Presentation

With the portfolio variations above in thoughts, it isn’t clear to me that Simon is as protected compared to Macerich because the valuation distinction suggests. Seeking to Tanger Manufacturing facility Shops for one more reference level, it too is valued at almost 2x the a number of of Macerich. Tanger is decidedly riskier than Simon whereas buying and selling on the identical valuation. All indicators level towards materials valuation growth potential for Macerich.

Funding Case

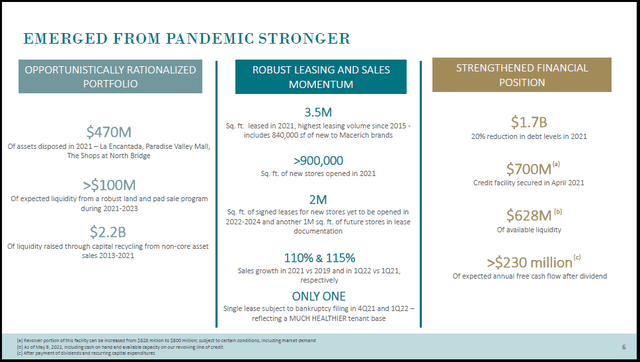

Macerich possesses the important thing elements for a superb actual property alternative: high-quality belongings at a reduced value. The next slide presents a common overview of current tendencies and Macerich’s present monetary place. The corporate seems to have ample liquidity at over $600 million whereas producing $230 million of disposable free money circulate after the dividend fee.

Macerich Investor Presentation Second Quarter 2022

With a market capitalization close to $2.4 billion, Macerich is paying a 5% dividend with a further 10% of disposable free money circulate. A 15% free money circulate yield on top-quality actual property is an uncommon alternative in the actual property sector.

Technicals

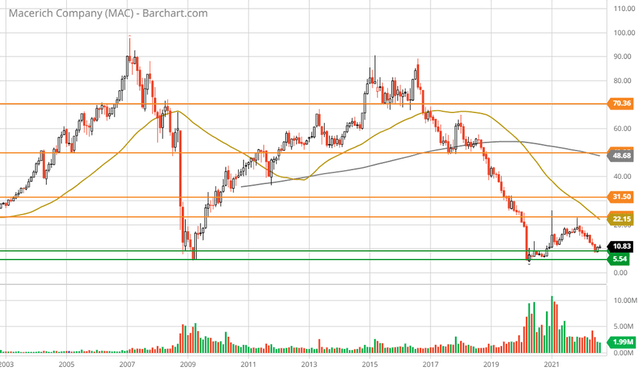

The technical backdrop is a mirror picture of the basics mentioned above. For Macerich, it’s best to start out with the massive image. On the 20-year month-to-month chart under, discover that Macerich has carved out a well-defined buying and selling vary with monumental amplitude (roughly $5 to $70).

Macerich 20-year Month-to-month Chart (Created by Brian Kapp utilizing a chart from Barchart.com)

The shares are presently testing the decrease finish of this vary and are nearing ranges solely seen throughout market panics, the GFC and COVID. Please word that the orange strains signify resistance ranges and the inexperienced strains signify the first help zone. Macerich is presently discovering help on the higher inexperienced line. The next 5-year weekly chart offers a more in-depth look.

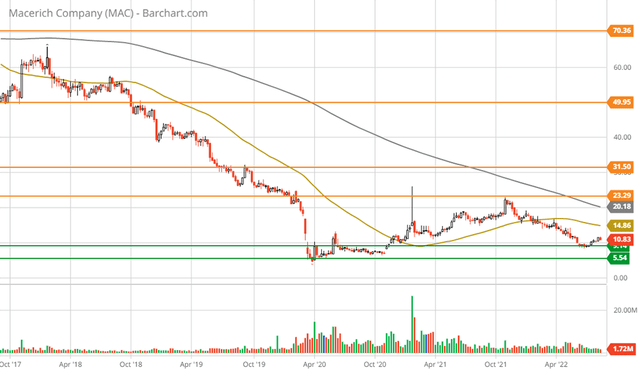

Macerich 5-year Weekly Chart (Created by Brian Kapp utilizing a chart from Barchart.com)

I might estimate that Macerich might be roughly confined to the zone outlined by the primary help and resistance strains for the foreseeable future, or $9 to $22. With the shares buying and selling close to $11, the technical asymmetry is clearly to the upside.

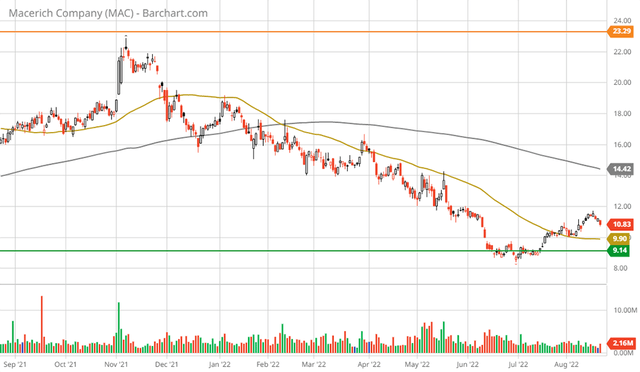

The second resistance stage simply above $30 is a potential value goal for the longer term, nevertheless, it seems unrealistic nearer time period given the state of the Retail REIT business. The 1-year day by day chart under offers a more in-depth take a look at the Macerich alternative. Please word that the gold trendline represents the 50-day shifting common, which is close to $10 presently. The gray trendline close to $14 is the 200-day shifting common and serves as a pure goal space.

Macerich 1-year Each day Chart (Created by Brian Kapp utilizing a chart from Barchart.com)

The value zone between $15 and $16 is prone to provide the primary materials resistance if an uptrend is to unfold. This value vary represents a excessive likelihood commerce alternative previous to heavier resistance close to $22.

Abstract

Macerich’s above-average threat is counterbalanced by the standard of its portfolio, discounted valuation, and robust technical setup. The chance/reward asymmetry is skewed to the upside, thus receiving a constructive score.

For these on the lookout for distinctive progress alternatives, the valuation growth potential is materials. For these on the lookout for progress and revenue, the revenue is above common for the fairness markets at 5% and is aggressive within the Actual Property sector general. Macerich possesses the important thing elements for a terrific actual property alternative: high-quality belongings at a reduced value.