Bet_Noire/iStock through Getty Pictures

Introduction

PARTS iD (NYSE:ID) launched its annual report for 2021 this week. Though gross sales went up virtually 12% from the earlier 12 months, the earnings from operations was unfavourable due primarily to elevated prices in commercial and provide chain disruptions.

Alternatively, the overall addressable market (TAM) is gigantic for a small firm like PARTS iD. This text will analyze whether it is in a superb place for attacking it and scaling its operations.

Whole Addressable Market

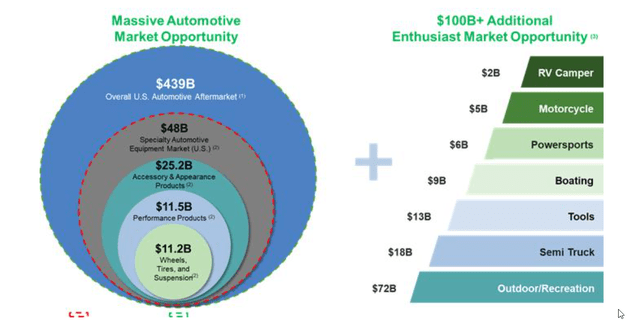

The annual report factors out that in accordance with Hedges & Firm, your complete automotive aftermarket and auto care trade might be $439 billion in 2022. PARTS iD has been traditionally centered on specialty automotive gear, with an estimated market of $48 billion. However it’s concentrating on to develop by means of automotive repairs, worldwide enlargement, and the addition of recent verticals. In any case, with Income throughout 2021 of $448.7M, there may be nonetheless a protracted option to develop to $48 billion (100 occasions).

TAM PARTS iD (PARTS iD 10-Okay FY2021)

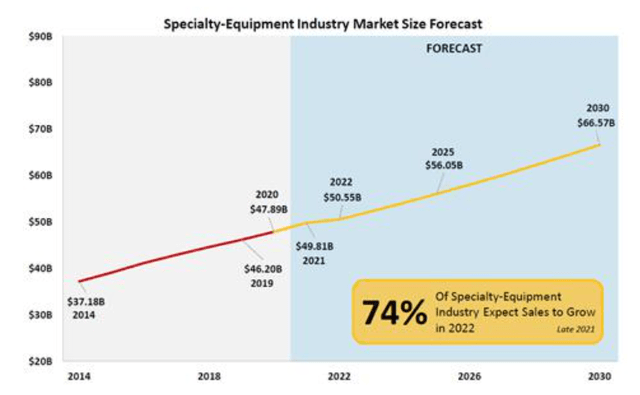

The special-equipment trade isn’t anticipated to develop spectacularly. Based mostly on the SEMA Future Traits January 2022 Report, round 3% yearly until 2030.

Specialty-Gear Trade Market Dimension Forecast (PARTS iD 10-Okay FY2021)

However what is important for PARTS iD can also be the penetration of eCommerce into this phase. In accordance with Hedges & Firm, the annual development price for elements eCommerce is projected just below 9% by means of 2025. They anticipate it to succeed in $38 billion in 2022 within the US.

Key Elements

Jeff Bezos has usually talked about the three vital elements in on-line retail that will not change sooner or later. They’re providing an unlimited choice, quick supply, and value. However within the case of this specific phase, we even have to think about the necessity for technical help. Whether or not in figuring out which particular half to purchase or which different complementary options require the set up, the shortage of technical help can stop the sale.

Alternatively, the well-known saying in industrial Actual Property investments is that the three extra vital elements are location, location, and placement. We are able to translate this to natural visitors, natural visitors, and natural visitors in eCommerce. If no person visits your retailer, then regardless of how great it’s, you will not get any gross sales. Paid visits are an alternative choice, however they value cash and would not scale.

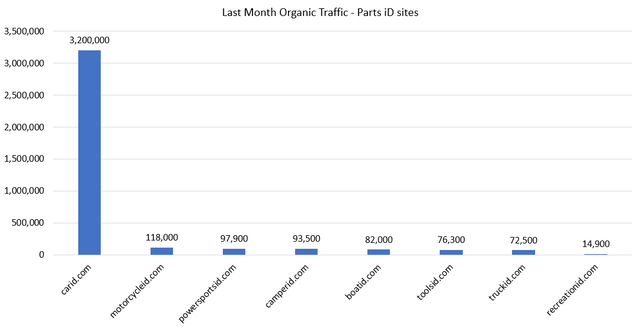

Beneath we are able to see the natural visitors of the completely different PARTS iD websites throughout final month.

Comparability of Final Month Natural Visitors – PARTS iD Websites (Created by the creator with Ahrefs data)

Though the natural visitors of the opposite seven verticals is rising sharper, carid.com is presently the main income generator with a giant distinction. So I’m going to focus this text on this phase.

Rivals

Analyzing the automotive equipment phase, we are able to discover three completely different sorts of on-line opponents: generalist eCommerce websites, different particular on-line retailers, and brick-and-mortar opponents with on-line shops.

Generalist eCommerce websites

Like Amazon (AMZN) or eBay (EBAY), wide-purpose websites promote among the similar merchandise PARTS iD gives. Their catalog is gigantic, and also you would possibly discover many particular elements. However these websites should not constructed particularly for the auto elements or comparable advanced segments (boats, leisure automobiles, and many others.). In order that they lack the precise search performance (the place you possibly can filter by 12 months or mannequin, for instance), the proposal of elements required for an set up, or specialised help.

So, even getting a share of this market, I do not suppose they may compete in the identical enviornment. And, given their dimension, it would not appear economically worthwhile for them to regulate their websites to take extra share of this area of interest.

Different Specialty On-line Retailers

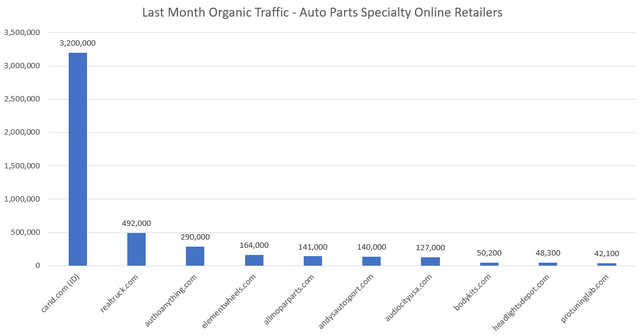

The web auto elements phase is a really fragmented market. Analyzing the natural visitors of the final month by means of Ahrefs, I’ve discovered the next figures.

Comparability of final month Natural Visitors – Auto Components Specialty On-line Retailers (Created by the Writer with Ahrefs data)

Ahrefs, a instrument for website positioning professionals, permits figuring out on-line opponents based mostly on the key phrases used within the searches. As we are able to see within the determine, PARTS iD is the chief on this particular market with many small opponents.

Being the chief in a fragmented market means having extra assets for competing higher and outgrowing them. Furthermore, it additionally implies that many purchasers already acknowledge its place and can come again to their web site or unfold its use. By 2021, 38.4% of the Income of iD has come from recurrent prospects.

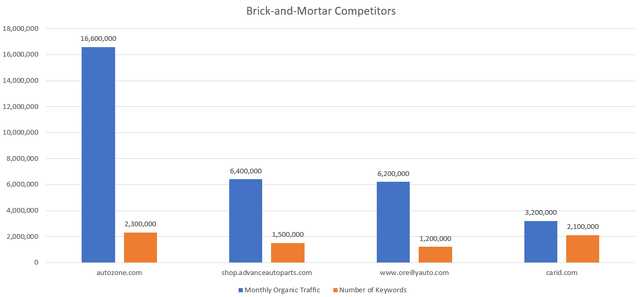

Brick-and-mortar Retailers

Lastly, some massive corporations have owned many vehicle half shops across the US and a few, even internationally, for years. They have been working earlier than the arrival of eCommerce, so their enterprise mannequin is a conventional one. However they’ve already created their web sites from which they’re already promoting elements. The principle ones are O’Reilly Automotive (ORLY), AutoZone (AZO), and Advance Auto Components (AAP).

In my view, these are the most important problem for PARTS iD. They’re already consolidated, specialised on this phase, and have important assets for growing and bettering their web sites.

Though they supply further elements varieties and providers to those supplied by PARTS iD, in complete, the three presently have extra month-to-month natural visitors.

Comparability of Final Month Natural Visitors – Brick-and-Mortar Rivals (Created by the Writer with Ahrefs data)

The variety of key phrases is the variety of completely different phrases entered within the search engine to reach at every web site. This determine is necessary as a result of it can provide us an concept of how the potential patrons come to every of them.

One factor to think about is that PARTS iD (with its web site carid.com) has extra key phrases than Advance Auto Components and O’Reilly, and it’s near AutoZone, presently absolutely the chief. This tells us that PARTS iD is getting visitors from a greater diversity of key phrases, even with fewer visits in complete than these opponents. The explanation have to be that carid.com is publishing extra particular content material, which in a technical area of interest like this would possibly lead to recurring visits sooner or later.

It’s tough to say how this market and this wager will evolve. However what is evident is that PARTS iD, with round 18.2M of various elements, and a technique the place the eCommerce is, no doubt, its core enterprise, is in a wonderful place to disrupt these current incumbents extra dispersed in logistics, bodily points, and conventional worthwhile mannequin.

Enterprise Mannequin

One of many important variations between PARTS iD and the massive brick-and-mortar rivals is that PARTS iD doesn’t maintain stock. It acts as an middleman negotiating with its distributors the drop transport on to prospects.

This enterprise mannequin has two important benefits. First, the capital employed is way decrease. In reality, the working capital of iD is unfavourable. Permitting it to have extra assets to develop and escalate. And second, there is no such thing as a limitation on the variety of references to be bought. What is expounded to the vital driver of an unlimited choice, which Bezos factors out.

The CEO, Nino Ciappina, talks about the potential of rising into different specialty areas, similar to they did with the seven verticals. Simply tweaking the platform, developed on-site for ten years, they might adapt it and launch it for different particular segments in an affordable period of time.

Professionals and Cons

To summarize, we are able to say that PARTS iD is an agile competitor with massive optionality in a mature market not but disrupted by eCommerce. Its enterprise mannequin will enable it to develop if it may possibly seize the rise in demand. And it’s in a superb place for diversifying into different specialty segments. Nino Ciappina, CEO of PARTS iD, says that certainly one of them, EV elements, is anticipated to generate extra equipment demand than oil automobiles. Nonetheless, he would not cite any supply which corroborates this affirmation.

In regards to the cons, we have to think about the likelihood that the massive brick-and-mortar opponents enhance their platforms, stealing market share from PARTS iD. Ultimately, their capitalization is way larger, so that they have extra assets to put money into them. Other than that, these opponents have already got a buyer base who might persist with them in case of going surfing.

We additionally have to level out, as a weak point, that there aren’t any important entry obstacles. It’s true that getting the seller agreements for providing greater than 18M items and putting in a platform for promoting and managing their logistics isn’t trivial. However there may be not but a large model recognition, a patent, or another aggressive benefit defending these gross sales.

Lastly, as stated firstly of this text, one particular attribute of this phase is the necessity for human help to assist customers discover the suitable half and knowledge for its set up. If this human help can’t be automated or requires important experience, it may possibly make this enterprise not so scalable because it sounded. There are at all times methods of reducing the price of this help, however whether it is, because it appears, a vital issue, it should present a substantial diploma of high quality, so prospects return.

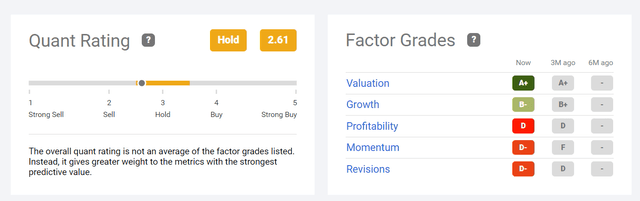

From a quantitative perspective, we are able to test the quant charges supplied by Searching for Alpha. Even being the general ranking solely Maintain, we’re speaking a couple of inventory with appreciable potential for Progress (ranking B-) and on the similar time scoring the utmost in Valuation (ranking A+). Each scores for a similar firm should not be straightforward to search out, as normally, the worth ought to replicate this potential.

After all, I would love it additionally to rank so effectively in Profitability and Momentum, however then, for certain, the worth would have already rocketed.

Quant Ranking for PARTS iD (Searching for Alpha)

Valuation

It’s difficult to worth an organization of those traits. Nonetheless, I at all times prefer to get no less than a really tough estimate to see whether it is discounting an extreme development or one thing extra affordable. As it’s a new mannequin in a mature market, we should deal with it as a dangerous funding, using solely a tiny proportion of our portfolio.

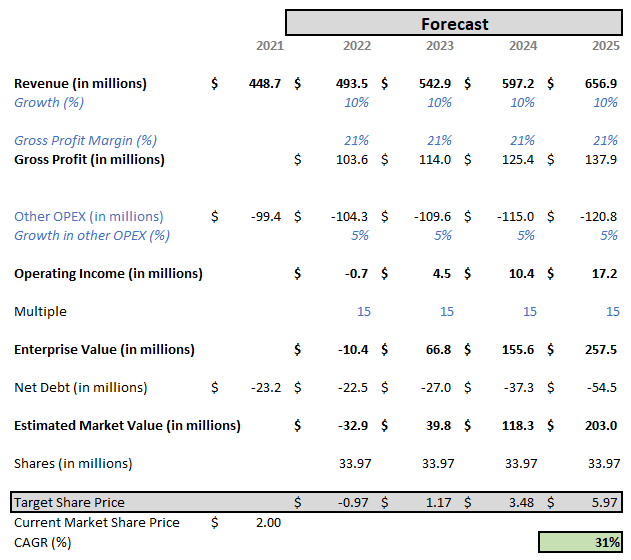

As stated firstly of this text, in accordance with Hedges & Firm, the compounded annual development price for elements eCommerce is projected just below 9% by means of 2025. Suppose we assume that PARTS iD will preserve its market share on this phase by means of this era and add some further development because of the sharper present improvement of the remainder of the verticals. In that case, we are able to forecast an annual 10% development in the course of the subsequent 4 years, which might make a income of $656.9M by 2025.

Within the final earnings name, Kailas Agrawal, CFO of PARTS iD, forecasted that they anticipate the Gross Margin to be between 23% and 23.5% within the subsequent 12 to 36 months. His primary argument is that PARTS iD has a capital-efficient just-in-time stock mannequin. As they do not carry inventory, they do not have a success value of their working bills. Along with that, they’ve launched some initiatives similar to transport value, vendor, and value optimization; adjoining vertical margin enhancements; and elevated personal label product gross sales. They have been averaging a Gross Margin of 21.4% within the pre-COVID period. Taking these phrases under consideration, but additionally that we’re in a world of inflation and provide shortages, we are able to assume, on a safer aspect, that this margin might be fixed with a price of 21% for the following 4 years. This margin will make a Gross Revenue of $137.9M by 2025.

As it’s a platform, the remainder of the Working Bills should not develop a lot because the Income. We do not know what’s going to occur with the average-per-click value, however we even have to think about some enhancements within the advertising course of and the remainder of the working actions. For example we assume an annual improve of 5% in these prices to get an Working Revenue of $17.2M by 2025.

Given the potential development of this firm, we’ll use a a number of of 15, which, when multiplied by the Working Revenue, offers us an Enterprise Worth of $257.5M. Including now the Internet Debt, projected with annually’s outcomes, we receive an Estimated Market Worth of $203M. After we divide it by the variety of shares (33.97M), we get a remaining valuation of close to $6. From the final market value ($2), this could symbolize a possible achieve of 300% or an annual achieve of round 30% till 2025. See the excel sheet with these calculations.

Tough Valuation – PARTS iD (Created by Writer)

Conclusion

PARTS iD is a disruption play in a mature market with low on-line penetration. As such, and particularly as enjoying in a disadvantageous place in regards to the massive incumbents, we have to deal with it as a dangerous funding.

However, then again, on the present value, it gives massive optionality, which may justify investing a small a part of our portfolio.