courtneyk

All males make errors, however man yields when he is aware of his course is flawed, and repairs the evil. The one crime is pleasure.”― Sophocles

At this time, we take an in-depth take a look at a widely known title within the housing sector. The current weak spot in housing exercise has triggered an approximate 20% decline within the inventory up to now in 2022. The shares now commerce at round 10 occasions earnings with a close to 4% dividend yield in addition to some current insider shopping for. An evaluation follows under.

Looking for Alpha

Firm Overview:

Headquartered in Denver, Colorado, RE/MAX Holdings, Inc. (RMAX) is the biggest actual property dealer on the planet, as measured by residential transaction sides (purchaser or vendor). It’s a 100% franchisor of each actual property and (extra lately) mortgage brokerage companies, boasting over 142,400 brokers in 110 nations as of March 31, 2022. RE/MAX was fashioned in 1973 and went public in 2013, elevating internet proceeds of $224.9 million at $22 per share. Its inventory at present trades round twenty 5 bucks a share, translating to a market cap of simply south of $800 million.

Enterprise Mannequin

The franchisor differentiates itself from different brokers by means of its working mannequin. Probably the most important facet of this mannequin is that its brokers normally obtain 95% of the commissions from a transaction versus 70/30 or 60/40 preparations typical of different brokerages. In return, RE/MAX franchisees pay mounted charges to share within the overhead prices of the brokerage and fund their very own advertising campaigns, both regionally or by means of charges to the franchisor that in flip go to assist model consciousness efforts. Along with offering better incentive to supply, this association permits brokers the flexibleness to barter fee charges with sellers, which may generally make the distinction when vying for an inventory. Owing to this mannequin, RE/MAX attracts productive full-time brokers, borne out by the truth that its U.S. brokers averaged 16.1 transaction sides in FY21, bettering second-place Realty Executives by 4 transactions, whereas doubling the output of different massive brokerages.

Whereas selling a extra entrepreneurial tradition for its brokers, RE/MAX doesn’t depart them out on an island, offering know-how instruments, together with a client going through app. It additionally requires every franchisee to attend a four-to-five day instructional seminar and gives agent assist by means of RE/MAX College, which incorporates downloadable movies and webinars. Moreover, being probably the most acknowledged title in actual property is a robust advertising device, leading to appreciable free referrals for its brokers.

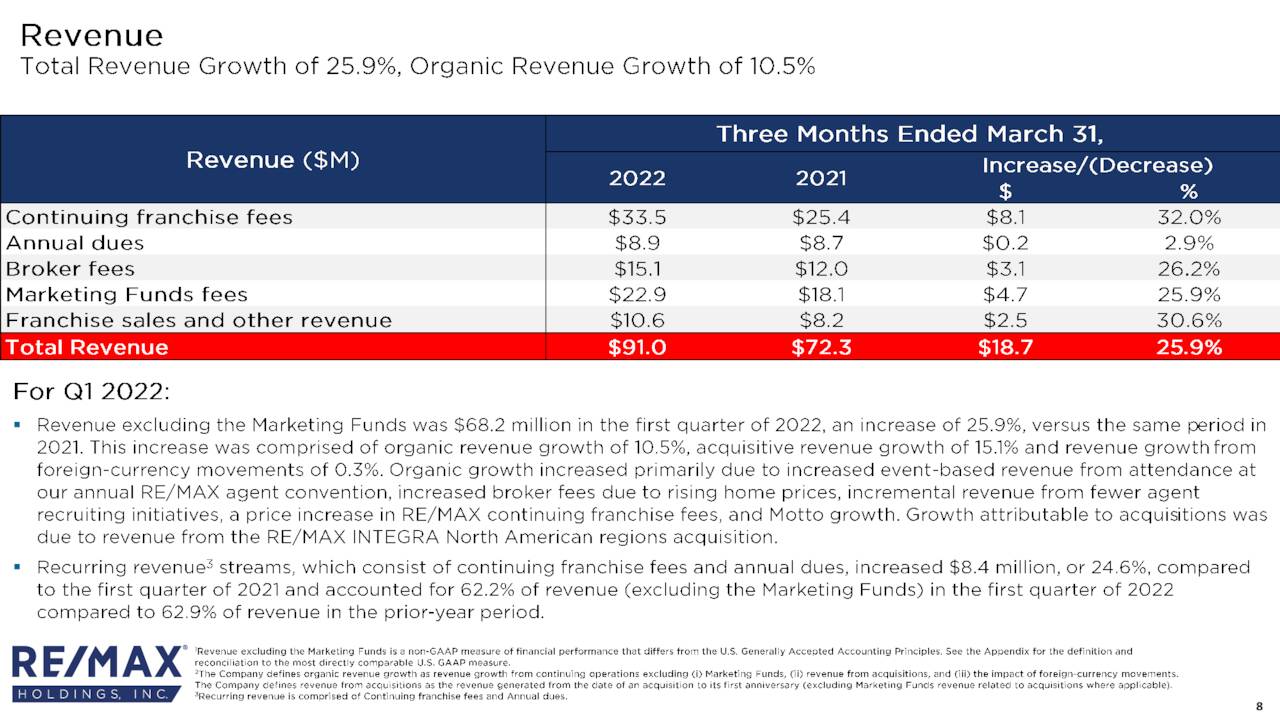

From this mannequin, RE/MAX receives 4 income streams: 1. month-to-month franchise charges – which quantities to ~1,550 per agent yearly; 2. annual dues of $410 from every of its U.S. brokers; 3. dealer charges from transactions; and 4. franchise gross sales. The primary two streams are a operate of the variety of brokers beneath its umbrella and accounted for 62% of the franchisor’s FY21 income. Brokerage charges delivered 26% whereas franchise gross sales generated the opposite 12%. It needs to be famous that the franchisor additionally receives advertising fund charges, which is its personal separate income line merchandise however is offset with the same expense line additional down the earnings assertion. It’s basically a value that’s charged to franchisees however should be acknowledged as income as a consequence of an accounting customary change in 2019. All references to income going ahead will exclude these advertising charges.

RE/MAX additionally has areas within the U.S. the place it has offered the regional franchise rights to unbiased homeowners, pursuant to which they’ve the unique rights to promote franchises in these areas. The economics are much less useful to RE/MAX in these locales and as such, it has employed a method to reacquire these rights – extra on this forthcoming. Along with the U.S. (60,717 brokers as of March 31, 2022), the franchisor has a big footprint in Canada (24,443 brokers) and is current in one other ~110 nations (57,245 brokers). That mentioned, the U.S. offered 81% of its FY21 high line, Canada 14%, with solely 5% coming outdoors these two nations. To additional belabor the purpose, its franchisor mannequin within the U.S. and Canada generated income of ~$2,900 per agent in FY21, whereas its unbiased territories contributed ~$800 per agent. Exterior the U.S. and Canada, RE/MAX solely averaged ~$200 per agent. It was these economics that compelled administration to buy unbiased proprietor RE/MAX INTEGRA in July 2021. For a consideration of $235 million, RE/MAX returned 9 U.S. states (~7,000 brokers) and 5 Canadian provinces (~12,000 brokers) into its fold.

Along with actual property brokerage, RE/MAX launched a mortgage brokerage enterprise in 2016 dubbed Motto Mortgage that operates beneath the same franchisor mannequin with 200 workplaces open within the U.S. as of July 7, 2022. With apparent synergies to buy mortgages necessitated by RE/MAX brokers, it generated FY21 Adj. EBITDA of damaging $5.3 million on income of $10.1 million Though its high line grew by 52% 12 months over 12 months, it nonetheless represented solely 4% of complete. Nevertheless, it ought to proceed its progress spurt and switch into the black throughout FY23. Supporting Motto is the franchisor’s fintech resolution named wemlo, which was bought in 2020. It’s a cloud-based, third-party mortgage processing platform designed for mortgage brokers, together with these outdoors the Motto community. To be used of the platform, RE/MAX receives charges on a per-file foundation. Administration believes that Motto and wemlo can finally generate $100 million in complete annual income.

Might Firm Presentation

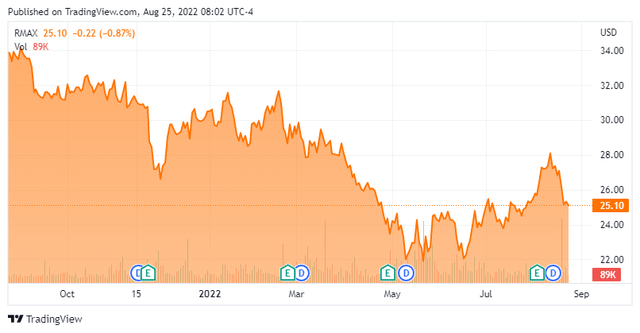

Inventory Value Efficiency

With secular tailwinds generated by a decade of low mortgage charges, the gradual southern migration of the Child Boomers, and customarily affluent financial situations, the true property market intrepidly climbed out of its Nice Recession hunch, with 2021 current residence gross sales up ~50% from their 2008 lows – though nonetheless under the report ranges of 2005 and 2006. The pandemic drove housing affordability to ranges not seen since 2014, however RE/MAX shareholders weren’t beneficiaries. After peaking at $67.50 a share in October 2017, their inventory has skilled a protracted decline to the mid-20s, aside from a quick accelerated detour under $15 in the course of the pandemic selloff.

There are a number of causes for this end result. First, RE/MAX was ridiculously overvalued. Its mannequin is pushed by agent progress and that metric is usually going to correlate with inhabitants progress. Even with increased than business common market share positive aspects, natural progress couldn’t be anticipated to climb into the double digits. (What number of actual property brokers does the world want?). However in October 2017, it was buying and selling at 44.7x FY18 EPS of $1.51 (GAAP), whereas from FY17 to FY21, its high line grew (predictably) at CAGR of 6% to $247.3 million.

Throw within the penetration of low cost brokers akin to Redfin (RDFN), in addition to the entry of iBuyers akin to Opendoor (OPEN), and the market additional discounted shares of RMAX, perceiving (eventually) an actual menace to the oddly and quasi-unbreachable actual property brokerage mannequin. That mentioned, 88% of all patrons and sellers in actual property transactions had been represented by a dealer in 2021 whereas the variety of licensed actual property brokers grew to a report ~2 million (roughly 1.6 million of that are members of the Nationwide Affiliation of Realtors). Both method, RE/MAX inventory has fallen over 60% from its all-time excessive in 2017 and 18% in 2022YTD, as a spike in mortgage charges has plunged housing affordability to its lowest stage since 2006, whereas the variety of energetic listings is down by roughly half from June 2019.

Latest Earnings:

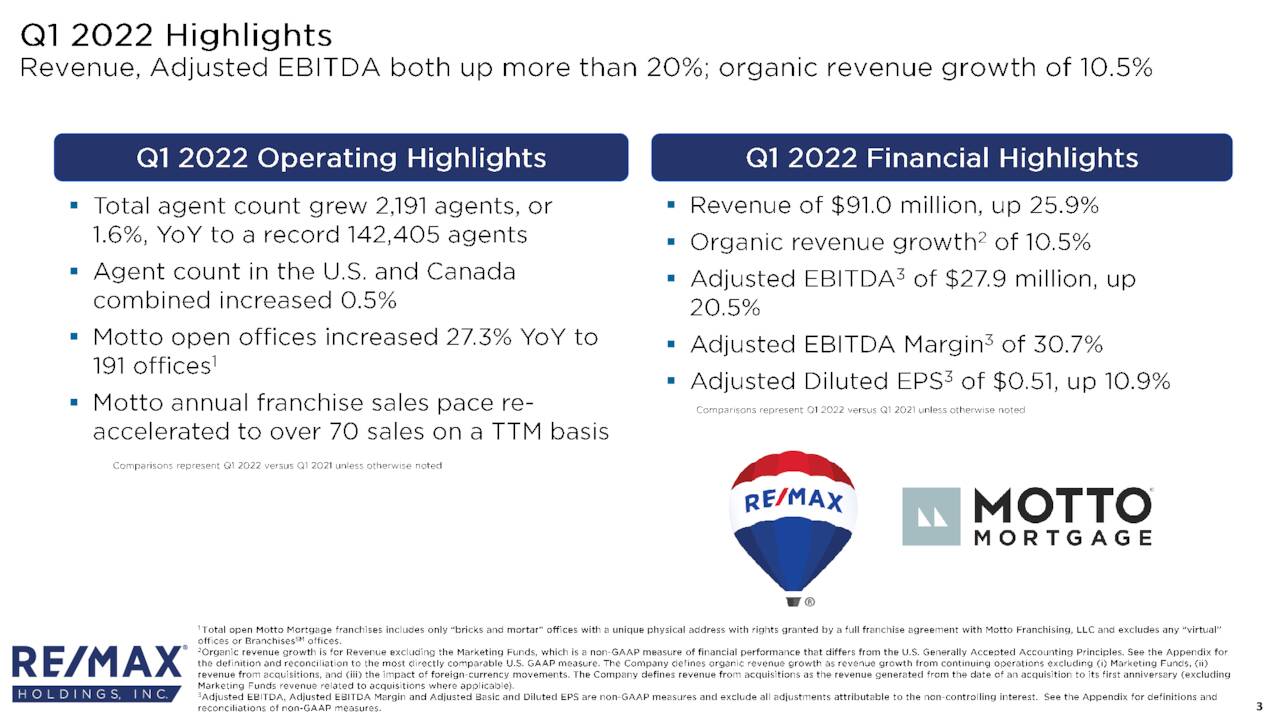

With these occasions unfolding, the franchisor reported 1Q22 earnings on April 28, 2022, posting EPS of $0.08 (GAAP) and Adj. EBITDA of $27.9 million on income of $68.2 million versus $0.06 a share and Adj. EBITDA of $23.2 million on income of $54.2 million in 1Q21, representing 33%, 20%, and 26% will increase, respectively. Nevertheless, RE/MAX INTEGRA was chargeable for ~60% of the top-line enchancment and earnings missed the Avenue consensus by $0.06 a share.

Might Firm Presentation

Administration projected YE22 agent depend up 3% to ~146,250, in addition to FY22 Adj. EBITDA of $132.5 million (up 11%) on income of $277.5 million (up 12%), all primarily based on vary midpoints.

Might Firm Presentation

On July seventh, the franchisor introduced a number of initiatives, together with inducements to transform competing brokerages to the RE/MAX community, accelerated funding in Motto Mortgage, and a 17% discount in its workforce (120 workers).

August Firm Presentation

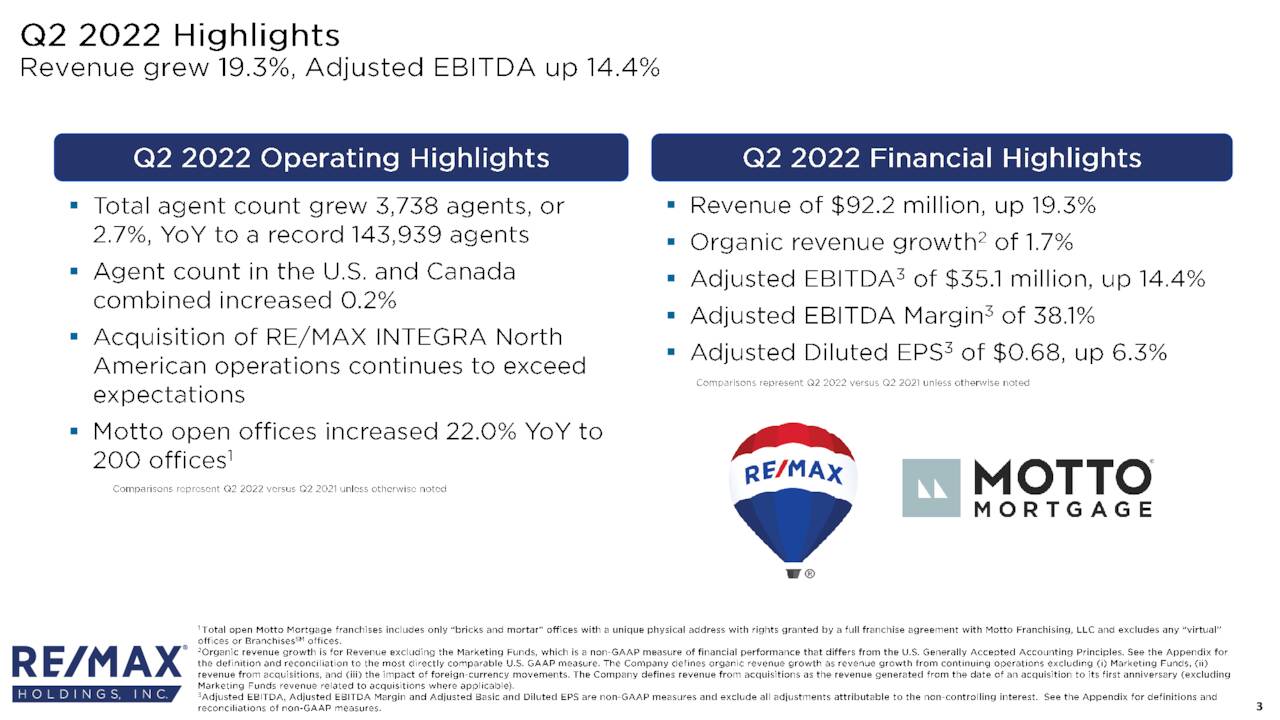

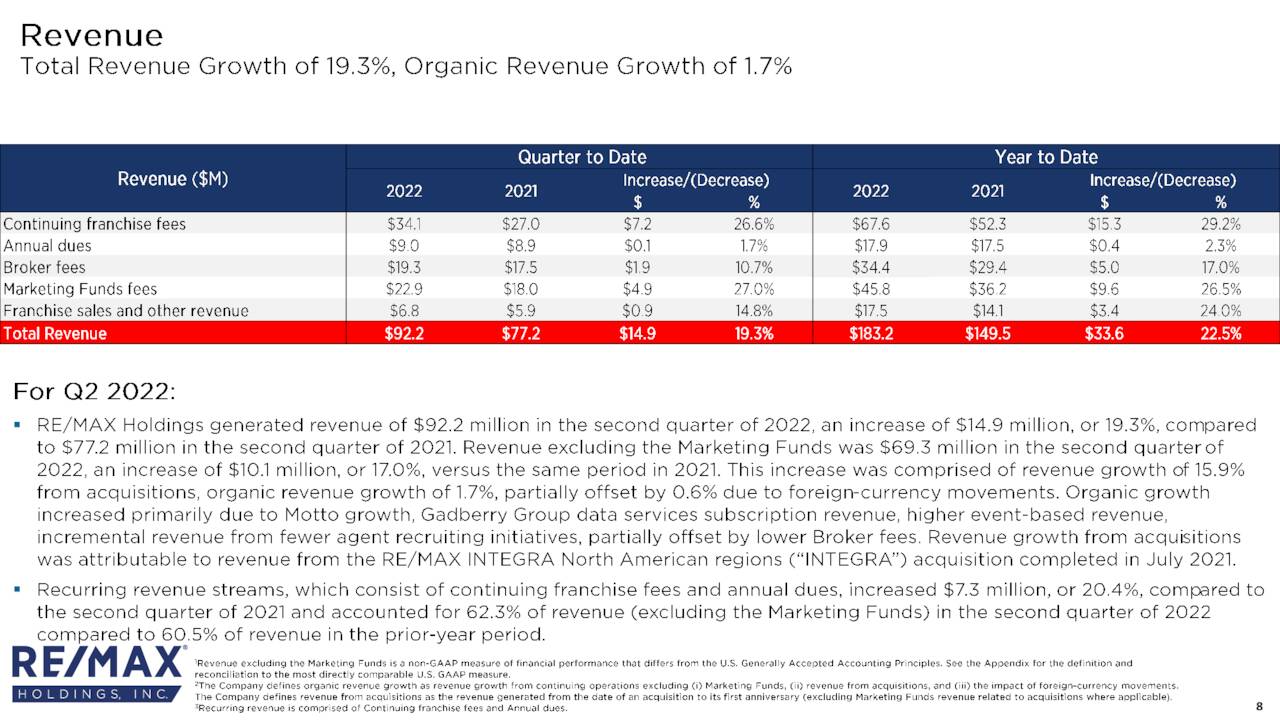

On August 4th, the corporate posted second quarter numbers. RE/MAX noticed revenues develop simply over 19% on a year-over-year foundation to $92.2 million as GAAP earnings got here in at 68 cents a share. Income was in line whereas earnings had been barely above expectations.

August Firm Presentation

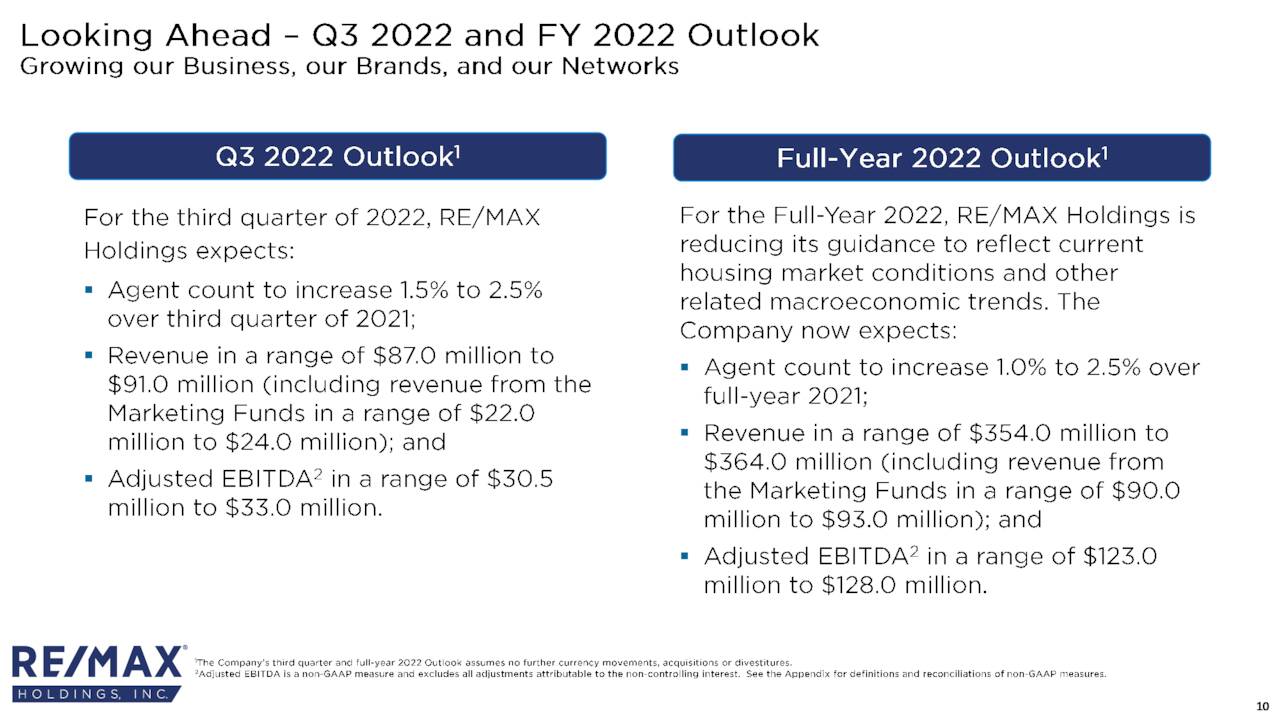

Administration did shave roughly $5 million at midpoint of the Q3 income ahead steering in addition to $10 million off FY2022 gross sales steering, which is now anticipated to be within the $354 million to $364 million vary.

August Firm Presentation

Steadiness Sheet & Analyst Commentary:

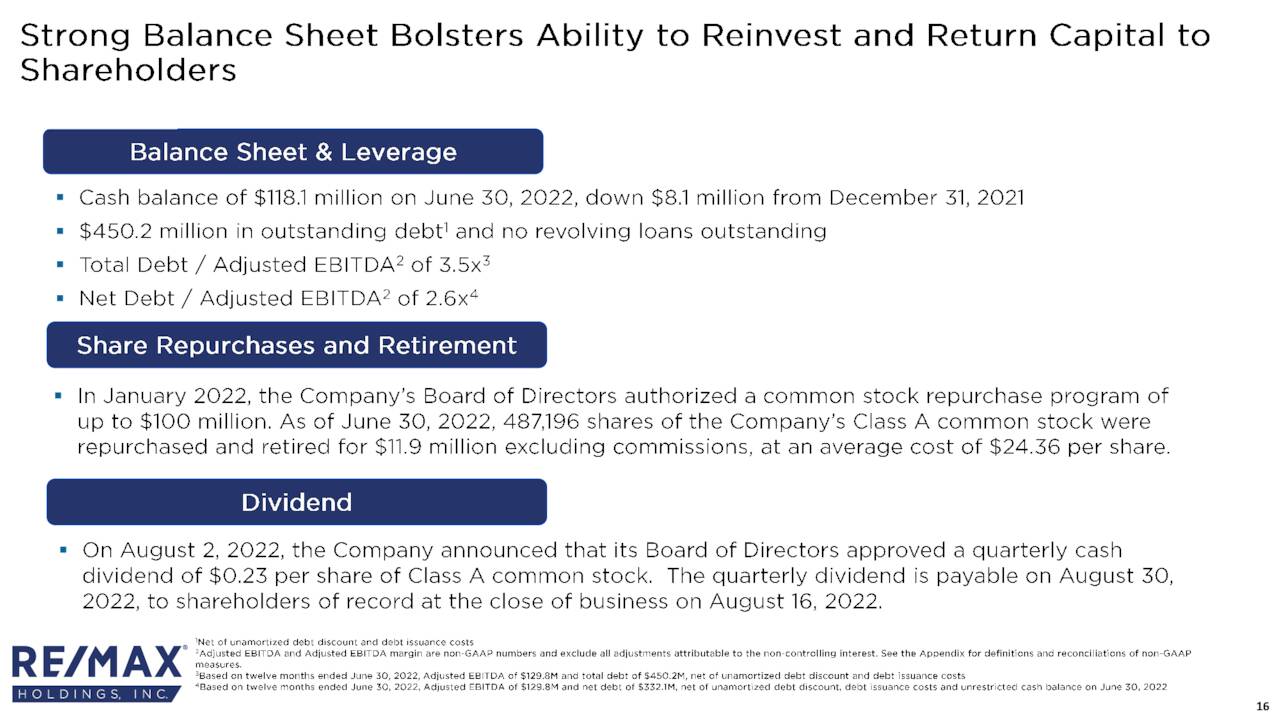

The lately introduced packages will likely be funded from assets available, which had been money and equivalents of $118.1 million as of the top of the primary half of 2022.. Debt was employed to finance the RE/MAX INTEGRA acquisition and stood at $450.2 million on the identical date, placing internet leverage at 2.6. RE/MAX pays a $0.23 quarterly dividend for a present yield of three.7%.

August Firm Presentation

It additionally introduced a $100 million share repurchase program in January 2022, of which some 12% has been executed by means of the primary six months of this 12 months. Money from operations, usually $70 million to $80 million every year, will likely be deployed to develop the agent depend, broaden Motto, pay its dividend, and repurchase inventory.

Solely 5 Avenue analysts have made commentary on RE/MAX up to now in 2022, cut up equally between two purchase and three holds, whereas their value targets starting from $28.00 to $38.00 a share. On common, they count on RE/MAX to earn simply over $2.40 a share on income of $360 million in FY22, adopted by simply over $2.50 a share on income of slightly below $375 million in FY23.

Helpful proprietor Adam Peterson stays bullish on RE/MAX’s future, buying 152,552 shares since mid-June, upping his possession curiosity to 11%

Verdict:

With solely roughly one-quarter of its high line transaction dependent, RE/MAX is extra insulated than different actual property brokers to downturns. And with its foray into mortgage brokerage significantly extra buy (than refi) dependent, the franchisor can be considerably shielded from sharp spikes in rates of interest. That mentioned, a 25-basis level enhance in mortgage charges reduces its full-year earnings by ~$0.03 a share, and with the unprecedented spike in charges over the previous six months, RE/MAX’s backside line will definitely be impacted.

Nevertheless, the collective yawn by the market over the previous three months – illustrated by its tight buying and selling vary across the low-to-mid 20s – to any information on this extremely risky financial milieu is suggestive of a backside being put in place. Buttressed by a share repurchase program, a 3.7% dividend yield, and a fast-growing mortgage brokerage franchise that ought to flip worthwhile in FY23, its share value is comparatively low-cost at simply over 10 occasions FY22E EPS, contemplating the quantity of regular money circulation it may well generate.

There may be an excessive amount of uncertainty within the housing market to extend publicity a lot to the sector at the moment. I consider RMAX could be a perfect coated name candidate given its valuation and excessive dividend yield. Sadly, there may be not sufficient liquidity within the choices towards the fairness to make that technique viable at the moment. Subsequently, I’ve taken a small “watch merchandise” within the fairness as I need to circle again on this title after the housing market stabilizes.

Generosity is giving greater than you possibly can, and pleasure is taking lower than you want.”― Khalil Gibran