Annual residence value appreciation has accelerated to file highs in every of the previous 12 months, after surpassing the mid-2000s housing-bubble excessive watermark of 11.9% in April 2021. [1] That run of data is more likely to finish quickly, because the housing market passes an inflection level. That doesn’t imply a housing crash is coming and even that costs will fall, however relatively that the tempo of value development is more likely to decelerate and extra houses will probably be obtainable on the market. This rebalancing can be welcome information for patrons, particularly these buying their first residence.

Rising stock

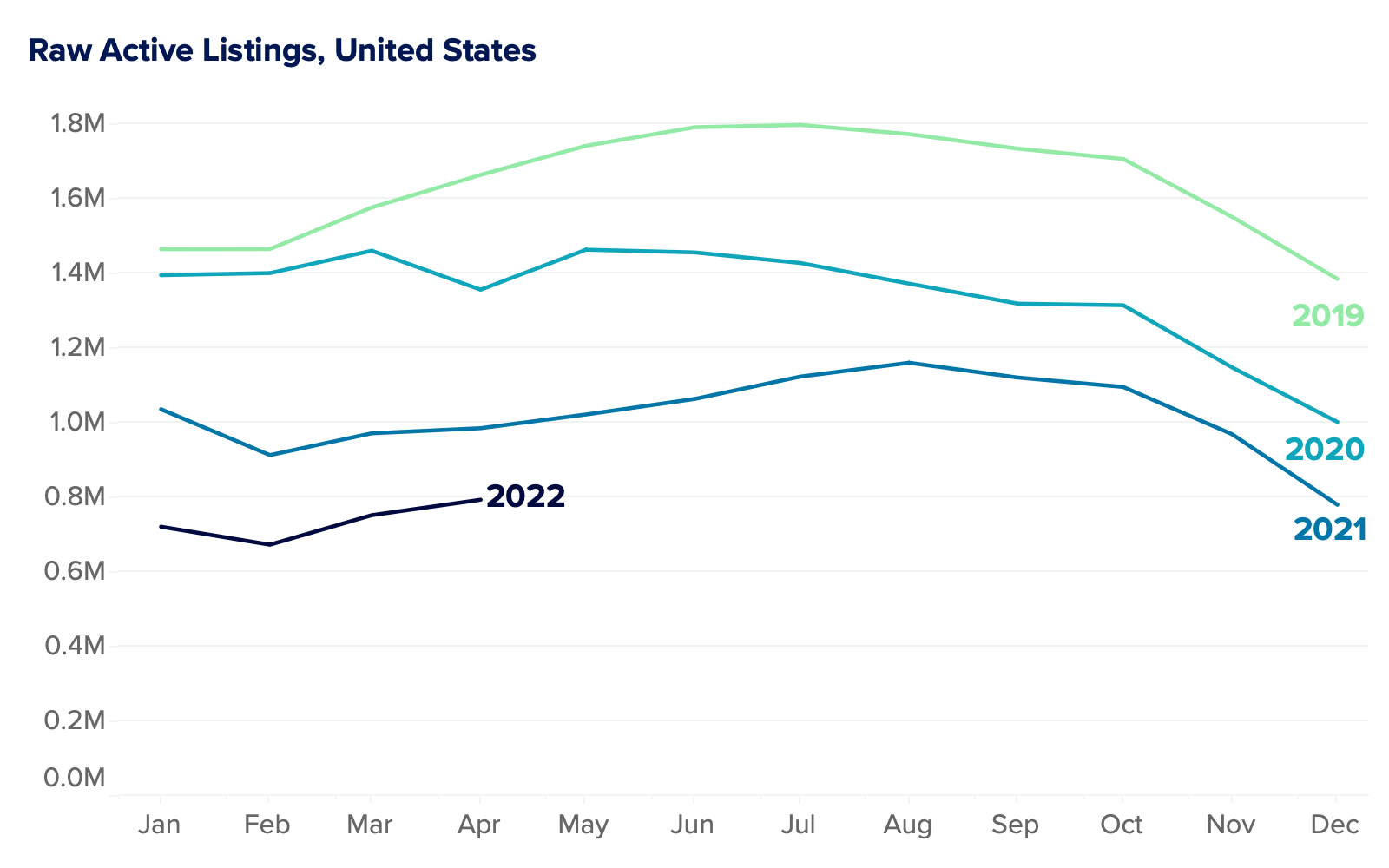

The extent of energetic stock is the housing market’s barometer, gauging the relative stress of demand versus provide. When demand persistently outstrips provide, the inventory of houses obtainable on the market is depleted. Like dropping barometric stress, plunging stock normally foretells stormy circumstances: sooner value development and sooner gross sales. That’s precisely what the market has delivered for the previous 12 months and a half.

Now, after months of plumbing file lows, stock lastly started to rise in March, not simply following seasonal traits however growing sufficient to start closing the hole with stock ranges of a 12 months in the past. It now appears to be like doubtless that stock will notch year-over-year development someday later in 2022, which hasn’t occurred since September 2019.

Extra stock is each the consequence and the reason for a extra balanced housing market: It offers residence consumers extra choices to select from — limiting the variety of patrons bidding on every residence — and lights a aggressive hearth below sellers and their itemizing brokers to make their houses shine, and to be cautious of overpricing. Stock could improve sufficient later this 12 months to sluggish the frenetic tempo of the market, as measured by the median residence vendor accepting a suggestion in simply six days thus far in April.

How far does it nonetheless should go?

The pendulum would possibly lastly be beginning to swing again towards a extra balanced housing market, however it’s going to take time to get there. And potential patrons nonetheless received’t discover a lot cause to cheer, as increased rates of interest will maintain homeownership pricey, and slowing value development is unlikely to finish with falling costs.

How lengthy would possibly it take? Nicely, even when stock reaches same-month 2021 ranges this summer time or fall, that may nonetheless go away stock down by about one-third from regular, pre-pandemic ranges. On the tempo of stock restoration noticed in March, stock would take about 30 months to achieve 2019 ranges. So circle September 2024 in your calendars to see if this extrapolation held true. [2]

In the event you belief the knowledge of crowds, verify with the roughly 100 housing market consultants surveyed by Zillow final quarter, whom we challenged with this very same query: 38% mentioned they anticipated stock to get well by the tip of 2024, narrowly edging out 2023 (37%) as essentially the most cited 12 months.

Is that this a bubble about to pop?

No, and in reality, the expectation of one other crash might contribute to retaining houses so unaffordable. Builders have been firing on all cylinders, and with extra houses below building than any time since 1973, they understandably really feel uncovered within the occasion of a housing downturn. In the event that they trim their building plans out of warning, we’ll miss out on top-of-the-line hopes we have now for web new stock available on the market, and the stock crunch that’s helped push costs up will persist for longer than anticipated.

If costs did start to fall, we all know there are hundreds of thousands of stymied first-time patrons, or youthful millennials quickly to be growing old into that state of affairs, ready within the wings to snap up houses in the event that they see a discount. These first-time patrons will proceed to really feel the stress from rising rents, which jumped 17% in simply the previous 12 months. And a usually high-inflation surroundings will maintain homeownership wanting engaging as a hedge towards inflation.

Most current owners are insulated from excessive mortgage charges, due to greater than 90% of loans prior to now a number of years being vanilla fixed-rate, absolutely amortizing mortgages. That retains individuals’s present payments reasonably priced, and can forestall a foreclosures wave just like the one which helped trigger the housing market to spin uncontrolled and crash in 2008. [3]

[1] U.S. Zillow Dwelling Worth Index, mid-tier, smoothed and seasonally adjusted. The pre-pandemic record-high annual appreciation was 11.9%, in October 2005, which was matched in April 2021 and has climbed once more each month till reaching 20.6% in March 2022.

[2] Relative to 2019 ranges, uncooked month-to-month stock for the U.S. rose from a 54.1% deficit in February to a mere 52.3% shortfall in March. A continuing tempo of an additional 1.77 proportion level discount within the hole towards 2019 ranges each month would take 30 months to achieve parity.

[3] City Institute Housing Finance: At a Look Chartbook, April 2022, p. 9: https://www.city.org/analysis/publication/housing-finance-glance-monthly-chartbook-april-2022