ADragan/iStock by way of Getty Pictures

The previous two years have seen immense volatility within the U.S housing market. As mortgage charges collapsed and other people made life-style modifications, dwelling gross sales skyrocketed. Unsurprisingly, this led to a surge in property costs, new dwelling improvement, and family debt. Moreover, many shares inside the actual property trade rose dramatically, together with the internet-based firm Zillow (NASDAQ:Z), which grew ~500% from its 2020 trough to its early 2021 peak.

I used to be one of many earlier skeptics of Zillow’s rally, as detailed in November of 2020 in “Zillow Group: Reversal Of ‘Housing Growth’ Creates A Brief Alternative.” My bearish thesis was that the housing increase would inevitably result in a crunch as soon as mortgage charges rise. Mixed with Zillow’s excessive debt because of its (now defunct) dwelling shopping for program and the truth that internet-based firms face extra important aggressive strain, it appeared to me that Zillow’s sky-high valuation was not wise. Generally, this thesis has confirmed right because the inventory is at the moment down by practically 50% because the article was revealed, and its buying-selling program has shuttered.

Is Zillow Lastly Buying and selling At Honest Worth?

After all, when any inventory is down 50%, it is a superb time to reassess its scenario to see whether it is lastly buying and selling at an affordable valuation. On the similar time, the corporate continues to face aggressive pressures and, extra importantly, skyrocketing mortgage charges have resulted in huge declines in dwelling gross sales. Whether or not or not the spike in mortgage charges causes a considerable and lasting crash within the property market stays “too be decided,” nonetheless, the macroeconomic backdrop has undoubtedly turned in opposition to Zillow’s favor. This shift has occurred at an inopportune second as the corporate is desperately trying to change its enterprise mannequin to maneuver previous its current missteps.

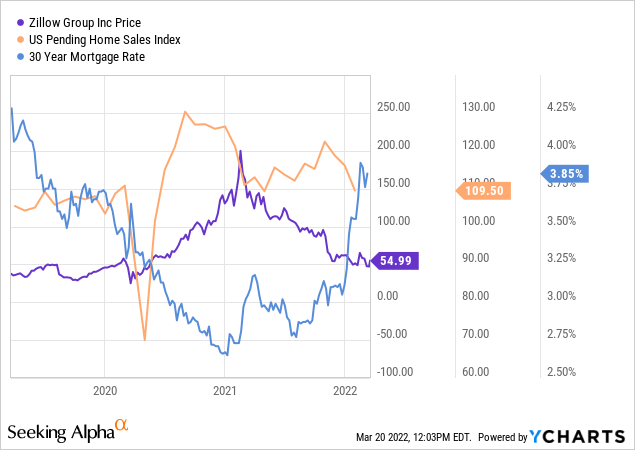

The corporate’s shifting macroeconomic backdrop might be seen within the inverse correlation between pending dwelling gross sales and common mortgage charges. When mortgage charges fall, extra houses are offered at larger costs. Once they rise, the comparative worth of renting over shopping for will increase, inflicting dwelling gross sales to say no. See beneath:

The steep tempo at which mortgage charges have risen is especially notable. This spike proceeded the current finish to the Federal Reserve’s colossal mortgage-backed-security buy program, which artificially held mortgage charges down and thereby supported the housing market. Since 2020, the Federal Reserve has been, by far, probably the most important mortgage financier available on the market. Now that the Q.E period has formally ended, bond liquidity has declined, because it seems non-public bond traders usually are not so keen to speculate at charges well-below inflation.

Accordingly, given the continued vitality disaster is ready to exacerbate additional inflation, mortgage charges might rise significantly larger earlier than reaching a brand new steady-state. Whereas inflation will not be immediately destructive for the housing market, its influence on mortgage charges might bankrupt many non-public mortgage lenders – mortgage REITs specifically. Problematically, as final seen in 2008, a decline in mortgage financier’s solvency might freeze the mortgage lending market, dramatically hamper dwelling gross sales volumes. On the similar time, rising gasoline and normal inflationary pressures leavings owners with decrease free disposable earnings, probably leading to larger default charges and decrease dwelling costs.

In my opinion, these are probably the most crucial bearish elements for Zillow because the firm’s gross sales are tied to mortgage and property agent referrals. If dwelling gross sales volumes decline and the market stays gradual for years, as I believe, then Zillow’s development potential is restricted. Happily, the corporate managed to dump the overwhelming majority of its “iBuy” houses, so its direct publicity to a possible decline in dwelling costs (because of rising charges) is much decrease than once I lined the corporate final.

Administration Modifications Offset Macro Losses?

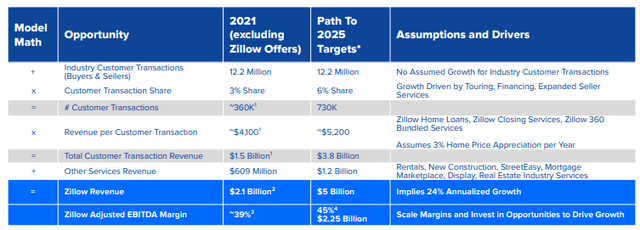

There may be all the time one other aspect to the coin. If its development technique works as anticipated, the inventory could also be buying and selling at a slight low cost right now. Not like mortgage REITs and residential builders, Zillow has a higher capability to make enterprise mannequin changes to stay afloat throughout occasions of turbulence. Moreover, as detailed in Zillow’s final investor presentation, 67% (12.2M) of all U.S dwelling patrons use Zillow right now, however, in 2021, solely 360K of these made “buyer transactions” with the agency. These embrace utilizing a “premier agent,” mortgage gross sales, or Zillow’s closing companies.

Zillow is at the moment leaving some huge cash and will see immense gross sales development by solely marginally rising the variety of whole prospects (12.2M) who make a transaction. Happily, the corporate has given a transparent mannequin for the influence of a rise in its buyer transaction share:

2025 Zillow Monetary Targets (Zillow Feb 2020 Investor Presentation)

In my view, these usually are not unreasonable estimates. Zillow has a strong buyer base and has emerged because the dominant supply for locating new houses. Given the comfort of discovering a realtor (and so on.) by their platform is probably going enticing to youthful homebuyers, rising buyer transaction share from 3% to six% over the subsequent three years appears possible. Thus, I might not be stunned to see a doubling of its whole income from now to then. Nonetheless, based mostly on my financial views relating to right now’s shifting property market, I believe Zillow may even see a decline in prospects as dwelling gross sales exercise declines. If the corporate can enhance buyer transaction shares sufficiently, this may occasionally not hurt Zillow’s income.

Nevertheless, I imagine that agent gross sales commissions will doubtless decline considerably beneath the normal 6% as demand for houses declines. Providers like Zillow that streamline and simplify the homebuying course of usually imply much less work for actual property brokers, notably a long time in the past when this work was all achieved by bodily mediums. Zillow’s market dominance on this trade might also be its detriment because of the potential for monopoly-power lawsuits and destructive strain on commissions. The actual property trade is among the many few the place commissions are nonetheless excessive, and Zillow capitalizes on acquiring a portion of these commissions. Whereas many have lengthy suspected that web companies will end in decrease commissions, I imagine it will solely happen as soon as there’s a bear market interval within the housing market as that will create a big “agent glut.”

There have solely been marginal declines in realtor’s commissions, so it might be a while earlier than this potential shift impacts the corporate. Nevertheless, it stays doable that each revenue-per-customer and whole prospects decline. The trick for Zillow will probably be to extend the share of paying prospects to those that “window store.” On condition that the precise ratio stays comparatively low, it appears doable that Zillow can undergo an actual property bear market with out shedding income and will even see income enhance regardless of it.

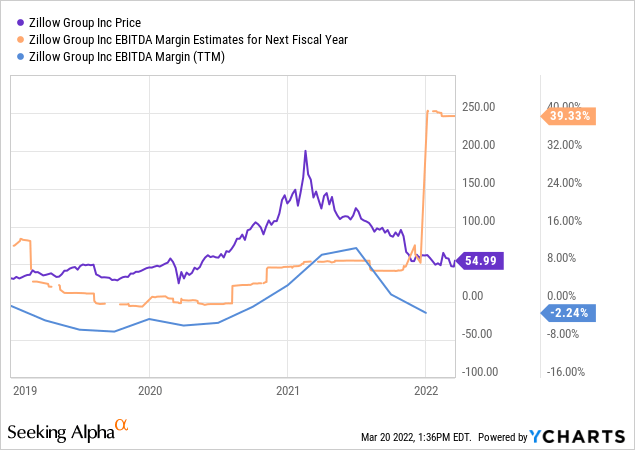

Nonetheless, Zillow has been unable to turn into persistently worthwhile. The agency has had destructive margins for years and has been extremely depending on debt development and fairness dilution to keep up its money ranges. After all, that is primarily because of its unprofitable dwelling flipping enterprise whereas its IMT section (which the corporate intends on rising additional) has had higher profitability. Nonetheless, there’s a clear pattern of Zillow’s EBITDA margin being beneath the anticipated worth:

The corporate believes it should see its EBITDA margins rise from near-zero to over 39% over the approaching yr. Given it’s not specializing in its money-losing section, this can be true, however I’ll nonetheless take this outlook with a grain of salt. The agency’s present consensus 2022 EPS estimate is $1.85 and as much as $3.45 by 2024. I imagine these estimates are possible, although, given the macroeconomic scenario, the strong anticipated 2022-2025 development is probably not really easy. It’s straightforward to correct in good occasions however way more tough when tides shift.

The Backside Line

I’m not firmly bearish on Zillow and wouldn’t guess in opposition to the inventory. After I lined the inventory final, its home-flipping enterprise gave it extreme publicity to the downturn in dwelling gross sales that will include rising mortgage charges. Nevertheless, Zillow’s administration was clever sufficient to reverse course and promote its dwelling property, commendably doing so (probably) at the cyclic peak of the U.S property market. Whereas a bearish shift within the housing market will nearly actually create points for Zillow, it has a higher capability to climate the storm than most.

Zillow’s path to profitability and better income is basically sound, however uncertainty stays very excessive. I believe that if there may be solely a minor slowdown in dwelling gross sales, Zillow might certainly develop its annual income to $5B by 2025. In my opinion, a extra important decline in houses gross sales akin to, however not essentially as dramatic as that of ~2007-2010, would doubtless upend Zillow sufficient to take away its development potential. If the actual property trade’s arguably extreme price construction lastly declines, then Zillow may even see some declines in gross sales because it goals to seize a lot of those charges.

At this level, I might not purchase Zillow’s inventory as I imagine it’s buying and selling close to its truthful worth. The corporate is at the moment buying and selling at a ahead “P/E” of 30X, and if its development expectations pan out and its EPS doubles from 2022 to 2025, then its long-term ahead “P/E” can be round 15X right now. Lengthy-term knowledge counsel mature firms have a tendency to commerce at a 15X “P/E,” although many “mature” corporations have traded at far larger valuations over the previous decade. Although I doubt Zillow’s development potential, they’re not robust sufficient to counsel that Zillow is considerably overvalued right now. Nonetheless, I’m solely keen to purchase a inventory if I imagine it’s dramatically undervalued, notably with uncontrollable financial threat elements akin to Zillow.