Patrick Chu/E+ through Getty Pictures

I will admit it is troublesome to go towards the grain and spend money on battered tech shares when it looks like all of the sensible cash is working the opposite means. Zillow Group, Inc. (NASDAQ:Z) has had its fair proportion of ache this 12 months. Alongside normal angst for tech and progress shares, Zillow can also be doubly dealing with the slowdown of the housing market, which is beginning to eat into the expansion charges of its flagship Premier Agent enterprise, whereas it additionally continues to work by way of a fancy wind-down of its iBuying technique.

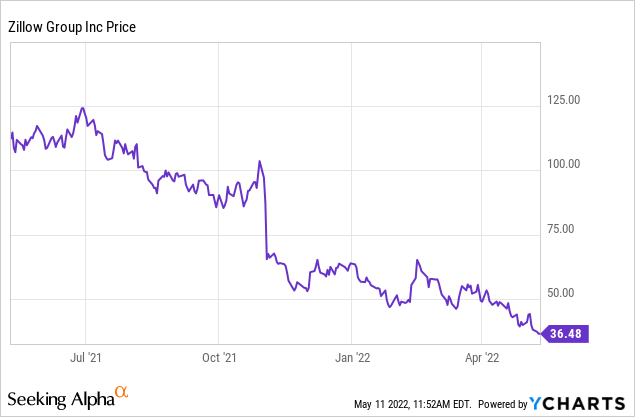

Zillow simply launched Q1 outcomes, and traders weren’t proud of the deceleration implied within the firm’s forward-looking steering. The inventory slipped ~10% immediately after earnings, with Zillow’s year-to-date losses now effervescent above 40%:

Sure, there may be noise right here: however can traders keep on with specializing in the long run? I stay bullish on Zillow, with this core precept in thoughts: the true property market will at all times have cycles, in the very same means the inventory market does. Buyers punishing Zillow for this pure seasonality is not sensible. As a substitute, deal with the larger image of the platform that Zillow is constructing to seize extra pockets share inside client actual property, and have faith in the truth that Zillow stays the most-visited actual property web site immediately.

Q1 obtain

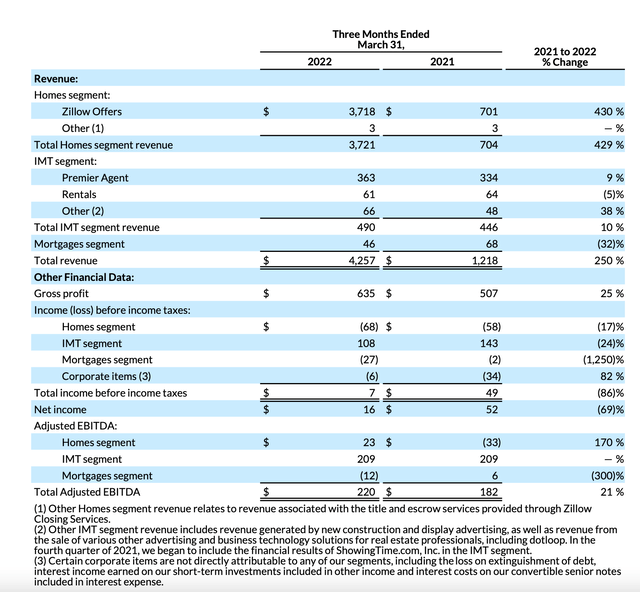

Let’s first give a fast recap on how Zillow’s enterprise carried out in Q1 and the purple flags that triggered the inventory value to drop. The Q1 earnings abstract is proven under:

Zillow Q1 outcomes (Zillow Q1 shareholder letter)

Now, with none context and searching simply at numbers, it might appear that Zillow is exploding. Income greater than tripled y/y to $4.26 billion, however you will word that the lion’s share of this got here from the $3.72 billion of income within the Houses phase. You will recall that final 12 months, Zillow made the selection to wind down its iBuying exercise and is unloading its portfolio of properties (a superb time to capitalize on still-high actual property costs as nicely).

The IMT phase, nevertheless, which is Zillow’s flagship enterprise and can be just about all of its income within the post-iBuying world, noticed income develop at 10% y/y to $490 million, which represents 4 factors of deceleration versus 14% y/y progress in This autumn.

Premier Agent income, in the meantime (the income minimize that Zillow takes when actual property brokers promote on Zillow), grew 9% y/y, additionally decelerating 4 factors from 13% y/y progress in This autumn, whereas rental income decayed -5% y/y. This was pushed by excessive occupancy charges within the U.S. and a slowdown in rental promoting.

Ditto for the mortgages phase: mortgages noticed a -32% y/y decline, pushed by the continued tightness of housing stock plus the slowdown in mortgage purposes resulting from sharply rising rates of interest.

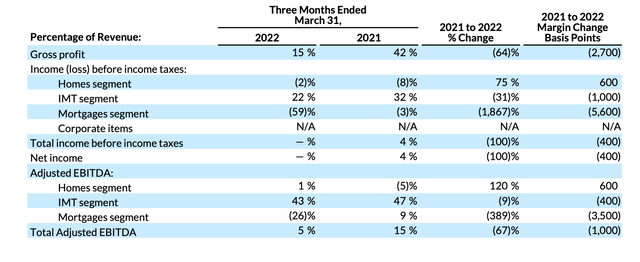

Pushed by decelerating income and the expertise investments that Zillow is constant to make into the IMT enterprise, IMT phase adjusted EBITDA margins peeled again 400bps to 43%:

Zillow Q1 adjusted EBITDA (Zillow Q1 shareholder letter)

Here is some extra useful coloration commentary from CEO Wealthy Barton’s ready remarks on the Q1 earnings name, detailing the dynamics the corporate is witnessing within the housing market:

Earlier than we get into our outcomes for the quarter, I might prefer to spend just a little time speaking concerning the housing market given it is on everybody’s thoughts. There’s a dispersion of actual property forecasts amongst publishing economists that vary from 5.5 million to six.5 million present dwelling gross sales for 2022 in comparison with 6.1 million in 2021. This ends in a transaction progress price vary of damaging 10% to optimistic 7%.

The frequent thread throughout these forecasts is uncertainty for the housing market. We proceed to see low ranges of stock down 23% year-over-year in March. New for-sale listings had been much less strained in March, up 36% from February ranges, however nonetheless down 9% year-over-year.

Common web page views per itemizing had been at a file excessive in Q1, which ends from low stock, sure, but additionally indicators a robust intent to maneuver. These dynamics drove dwelling values up an astonishing 21% year-over-year in March regardless of rising rates of interest, which, in fact, exacerbate affordability challenges.

So whereas we all know persons are nonetheless keen to maneuver, market circumstances are making it more and more troublesome. The web results of all of those elements is that complete client transaction worth progress tendencies are meaningfully softening and even probably the most revered prognosticators have disparate views of what’s going to occur subsequent.

Regardless of this turbulent housing market, Zillow is positioned because the chief on the prime of the true property funnel stands agency with 2.6 billion visits in Q1, together with a 38% distinctive customer progress year-over-year in leases based on comScore.”

Looking forward to the longer term

Okay, so that is what is going on proper now; however what concerning the future? Zillow continues to goal for targets of:

- $5 billion in income by 2025

- A forty five% adjusted EBITDA margin when it hits that scale, or ~$2.25 billion in annual adjusted EBITDA.

I will proceed to emphasise my normal thesis: whereas the true property market will at all times have its ebbs and flows, what traders must be grounded on is Zillow’s continued maintain over customers and the enhancements it is making to its platform.

The corporate continues so as to add new options that encourage home-buyers to take motion. In Q1, the corporate made enhancements to its digital home-touring expertise to mix photographs, ground plans, and spatial perspective right into a extra coordinated digital expertise. For in-person excursions, the corporate additionally added the ShowingTime Actual Time function in lots of markets, which provides precise instances that properties can be found for an agent tour.

Past this, here is a rundown of all the explanations I stay bullish on Zillow in the long run:

- Exit from iBuying shines the highlight on margin-rich IMT phase. In 2021, Zillow’s core IMT phase (which generates charges from actual property brokers discovering purchasers on the Zillow web site) noticed its adjusted EBITDA margins increase to 45%, up from 38% in 2020. That signifies a income stream that’s practically pure revenue and really minimal overhead, and immediately correlated with the uptick in actual property exercise. To me, eradicating the distraction from iBuying and its horrendous quarterly losses can have the impact of increasing valuation multiples for Zillow’s worthwhile core enterprise.

- Throughout Zillow, Trulia, StreetEasy, and Hotpads, just about each American client serious about shopping for or renting a house will come throughout one of many Zillow Group’s web sites. Zillow has constructed an ecosystem wealthy with actual property knowledge that has turn out to be the forefront of on-line actual property for customers. Zillow site visitors reached a file excessive of 10.2 billion visits (+6% y/y) in 2021.

- Zillow is a platform that may add a complete suite of extra monetizable companies. With all this site visitors, Zillow’s capacity to generate tertiary income is broad. At the moment, nearly all of Zillow’s enterprise comes from promoting charges paid by actual property brokers, however the firm can also be increasing into distributing mortgage merchandise as nicely. Sooner or later, Zillow might provide a full suite of “after-market” dwelling add-ons, together with home insurance coverage, transferring companies, furnishing/inside ornament companies, and others.

From a valuation perspective, it is a very engaging time to spend money on Zillow. At present share costs close to $36, Zillow trades at a market cap of $9.15 billion. After we web off the $3.63 billion of money and $1.74 billion of debt on Zillow’s most up-to-date steadiness sheet, the corporate’s ensuing enterprise worth is $7.27 billion.

Trying backward on the $853.2 million of adjusted EBITDA that the IMT phase generated in FY21 (ignoring the losses within the Houses phase, as we must always successfully consider that as discontinued operations going ahead), Zillow’s valuation is at 8.5x EV/trailing adjusted EBITDA. If we stay up for the corporate’s 2025 aim of $5 billion in income at a forty five% adjusted EBITDA margin ($2.25 billion), Zillow is probably presently buying and selling at simply ~3x its future EBITDA potential. There’s lots of room right here, for my part, for upside.

Key takeaways

Reap the benefits of the market’s latest worry to construct a long-term stake in Zillow. Trying forward, Zillow continues to be the dominant client actual property web site that enjoys the lion’s share of net site visitors. Its internet marketing/Premier Agent enterprise continues to be a prime advertising and marketing channel for actual property brokers, and the income stream is available in at a really excessive EBITDA margin already. Keep lengthy right here.